Qubit: Howard Marks on Investor Psychology

Qubit: Howard Marks on Investor Psychology

Howard Marks was interviewed on the Invest Like the Best podcast last year where he shared what three questions investors should ask themselves if they want to outperform:

Are you willing to be different?

Are you willing to be wrong?

Are you willing to look wrong?

Essentially, do you dare to do the things that you have to do to be great and are you willing to tolerate the discomfort to do so?

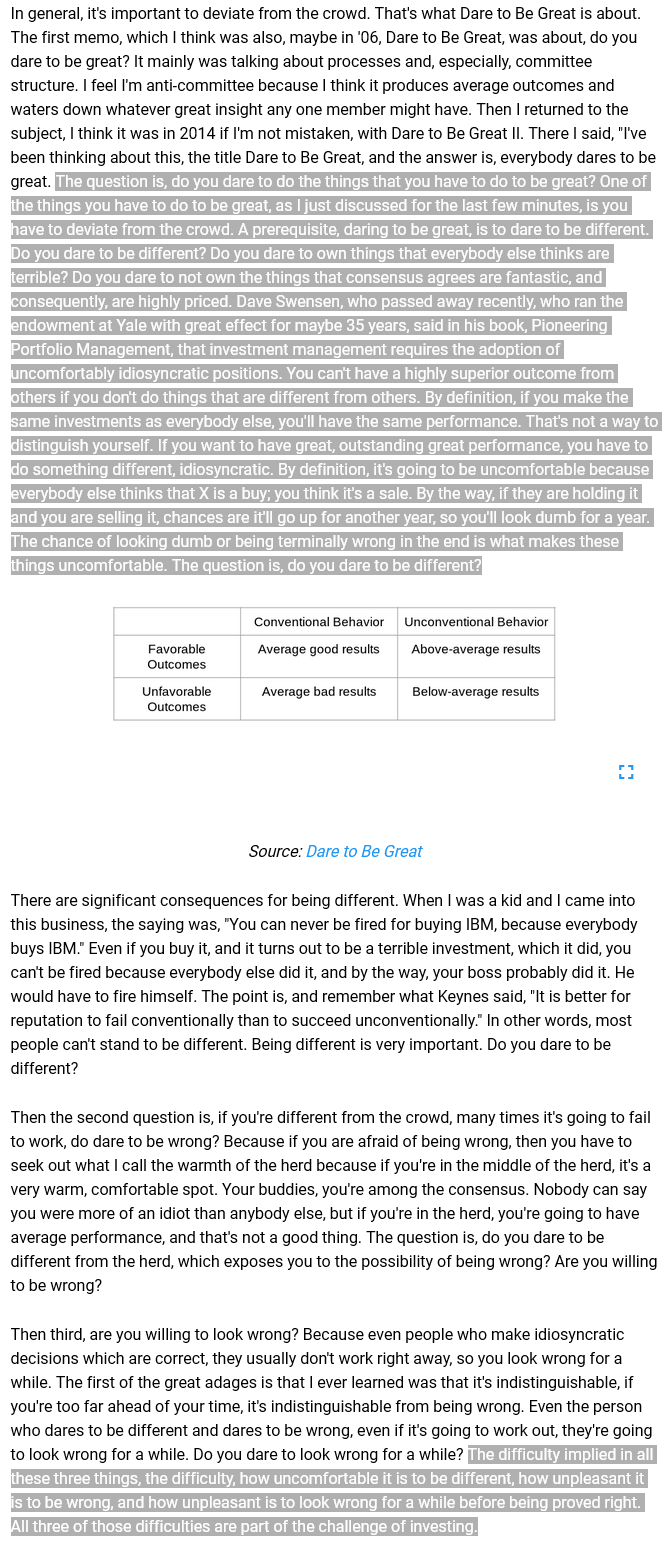

“The question is, do you dare to do the things that you have to do to be great? One of the things you have to do to be great, as I just discussed for the last few minutes, is you have to deviate from the crowd. A prerequisite, daring to be great, is to dare to be different. Do you dare to be different? Do you dare to own things that everybody else thinks are terrible? Do you dare to not own the things that consensus agrees are fantastic, and consequently, are highly priced. Dave Swensen, who passed away recently, who ran the endowment at Yale with great effect for maybe 35 years, said in his book, Pioneering Portfolio Management, that investment management requires the adoption of uncomfortably idiosyncratic positions. You can't have a highly superior outcome from others if you don't do things that are different from others. By definition, if you make the same investments as everybody else, you'll have the same performance. That's not a way to distinguish yourself. If you want to have great, outstanding great performance, you have to do something different, idiosyncratic. By definition, it's going to be uncomfortable because everybody else thinks that X is a buy; you think it's a sale. By the way, if they are holding it and you are selling it, chances are it'll go up for another year, so you'll look dumb for a year. The chance of looking dumb or being terminally wrong in the end is what makes these things uncomfortable. The question is, do you dare to be different?”

“Then the second question is, if you're different from the crowd, many times it's going to fail to work, do [you] dare to be wrong? Because if you are afraid of being wrong, then you have to seek out what I call the warmth of the herd because if you're in the middle of the herd, it's a very warm, comfortable spot. Your buddies, you're among the consensus. Nobody can say you were more of an idiot than anybody else, but if you're in the herd, you're going to have average performance, and that's not a good thing. The question is, do you dare to be different from the herd, which exposes you to the possibility of being wrong? Are you willing to be wrong?

Then third, are you willing to look wrong? Because even people who make idiosyncratic decisions which are correct, they usually don't work right away, so you look wrong for a while. The first of the great adages is that I ever learned was that it's indistinguishable, if you're too far ahead of your time, it's indistinguishable from being wrong. Even the person who dares to be different and dares to be wrong, even if it's going to work out, they're going to look wrong for a while. Do you dare to look wrong for a while? The difficulty implied in all these three things, the difficulty, how uncomfortable it is to be different, how unpleasant it is to be wrong, and how unpleasant is to look wrong for a while before being proved right. All three of those difficulties are part of the challenge of investing.”

Source

Howard Marks - Embracing the Psychology of Investing

Tweets and Posts:

Qubits are insights that we find and share with you.