Qubit: MITIMCo 15-Year Letter

Qubit: MITIMCo 15-Year Letter

Back in March MITIMCo published a 15-year letter to their alumni.

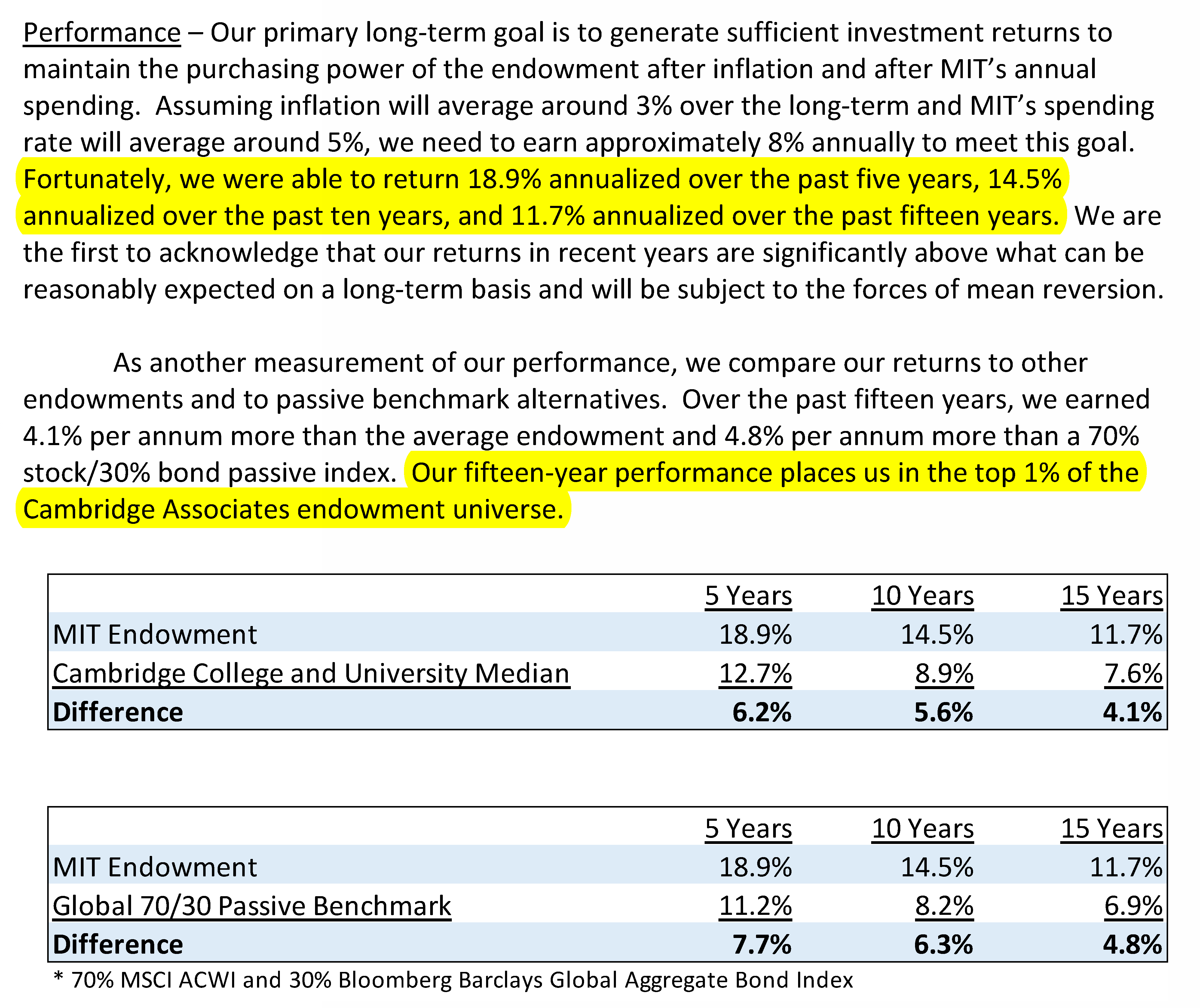

In the 15 years since CIO Seth Alexander took over the endowment at MIT, they earned an 11.7% annualized return as of FY 2021. The endowment was in the top 1% of the Cambridge Associates endowment university.

To achieve that, they had to change how and what they invest by exploring overlooked funds and becoming their first institutional LP.

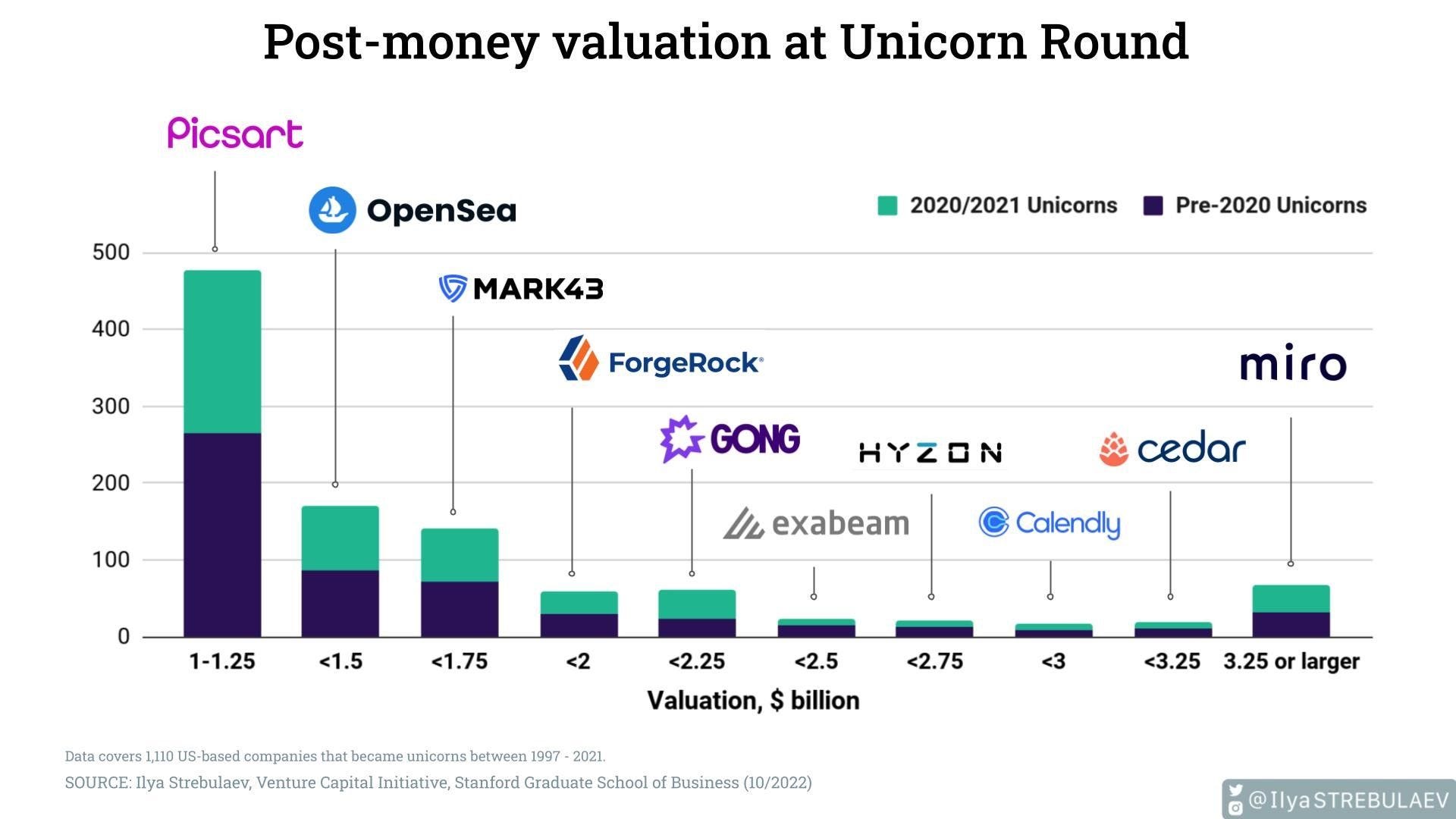

They also admit to missing out on late-stage tech, though that might turn out to be more a blessing now than a curse. Time will tell.

“We have tried to take a different approach in several areas. One example is our investment manager selection process. Historically, we sought out established firms with long track records of success. Such firms were easier to diligence, quick to get internal approval, and much less likely to result in disastrous return outcomes. Unfortunately, these firms also were harder to develop relationships with (due to numerous demands on their time), harder to garner capacity from (due to significant interest from other investors), and often facing headwinds to future investment success (due to larger asset bases and more complicated organizational structures.) As an experiment, we began to target smaller, more off-the-run managers such as brand-new firms, firms started by people who did not have ‘traditional’ backgrounds, firms delving into new arenas, firms with unusual organizational and fund structures, and any other type of firm that did not match the typical institutional playbook.

We discovered that we very much liked the arena of overlooked firms. By definition, there were fewer other investors competing for manager attention and manager capacity, giving us the opportunity to develop deeper, longer duration relationships. These managers also were more likely to be an outlier in some way – perhaps they had been forced to be innovative to survive or perhaps they simply viewed the world differently because they did not have the advantages of being an incumbent. Finally, they usually had less money under management than well-established firms and were hungry to succeed. Over the past five years, we have been the first institutional investor or among the first group of institutional investors in more than 50% of our new relationships.”

“One mistake we made in recent years was a failure to capitalize sufficiently on co-investments in late-stage venture capital companies. While pattern recognition is one of the great benefits of experience, overreliance on pattern recognition can be a hindrance to good decision making, particularly during periods of secular change. Based on our historical experience, we believed that late stage venture capital co-investments generally were poor risk-reward because that these rounds of fundraising often were priced by investors hoping for a quick gain in the IPO process and such transactions were likely to be pro-cyclical investments made at market peaks in the largest and least attractive of fund investments.

As a result of our pre-conceived notions, we were slow to recognize that the market environment had changed dramatically. The rise of bigger, winner-take-all global technology companies and the tendency of these companies to fund themselves longer in private markets created numerous situations in which MIT’s venture capital managers had access to compelling late-stage private investments that they wanted to share with limited partners. Instead of the negative selection bias we had experienced historically, the late stage venture co-investments offered by our partners in recent years were actually some of the most attractive investment opportunities around. By focusing too much on the historic base rate and not enough on the opportunity set in front of us, we missed opportunities to earn compelling returns for MIT in companies such as AirBnb, JD.com, and Stripe.

We should note that we generally do not consider missing out on successful investments as a mistake. Usually, someone else is better positioned to understand and access opportunities than we are and our lack of involvement is a sign of discipline, not lack of initiative. In many cases, missed opportunities are simply not our money to make. Here, however, we believe this set of missed opportunities falls into the mistake category. As an existing investor with some of the best venture capitalists in the world, we were well-positioned to access these opportunities and failed to do so.”

Source:

Tweets and Posts:

Qubits are insights that we find and share with you.