Qubit: Princeton Endowment Returns 2022

Qubit: Princeton Endowment Returns 2022

Princeton's endowment returned -1.5% for FY 2022. It paid out $1.5 billion to the school covering 65% of its operating budget.

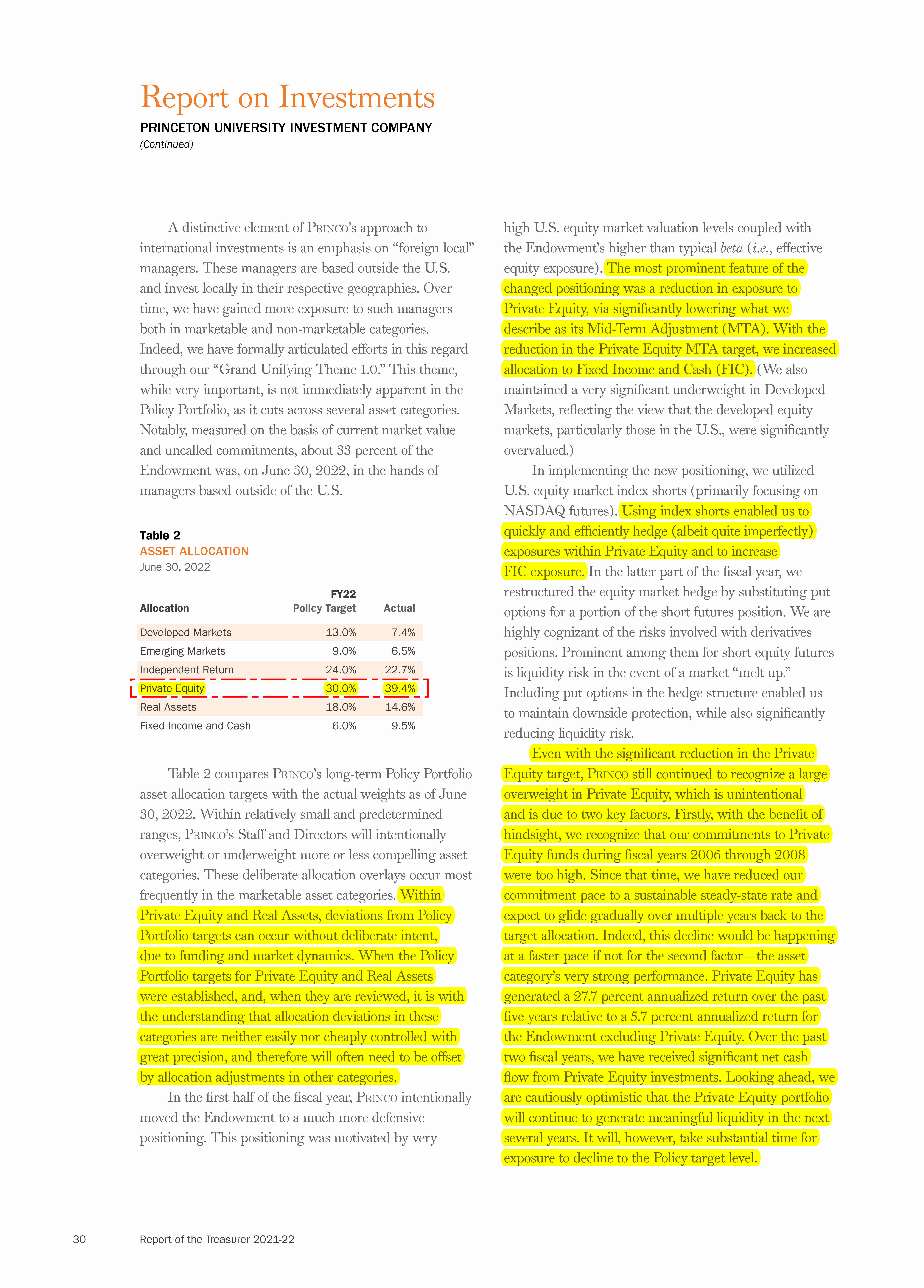

Curiously, the endowment reduced its exposure to its high allocation to private equity by using U.S. equity market index shorts. With that hedge the private equity asset class returned 7.6% for FY 2022.

But such a bet paying off might instill an inclination for similar short-term actions in the future that may hinder long-term performance.

“The portion of the Endowment actively managed by PRINCO generated a fiscal 2022 investment loss of 1.5 percent, outperforming its primary benchmark by 1.2 percent. Only once before in PRINCO’s history, in the midst of the Global Financial Crisis, have we produced a nominal loss. Yet we are quite proud of this year’s result. The loss is small compared to what might have been. Most markets around the world were down by double digits, as they reset from the bullish waves that abetted fiscal 2021’s blowout 46.9 percent return and broke into turbulent whitewater. Importantly, recent actions taken to radically shift the posture of our portfolio, including putting on a very large market hedge, were critical to preserving last year’s gain.”

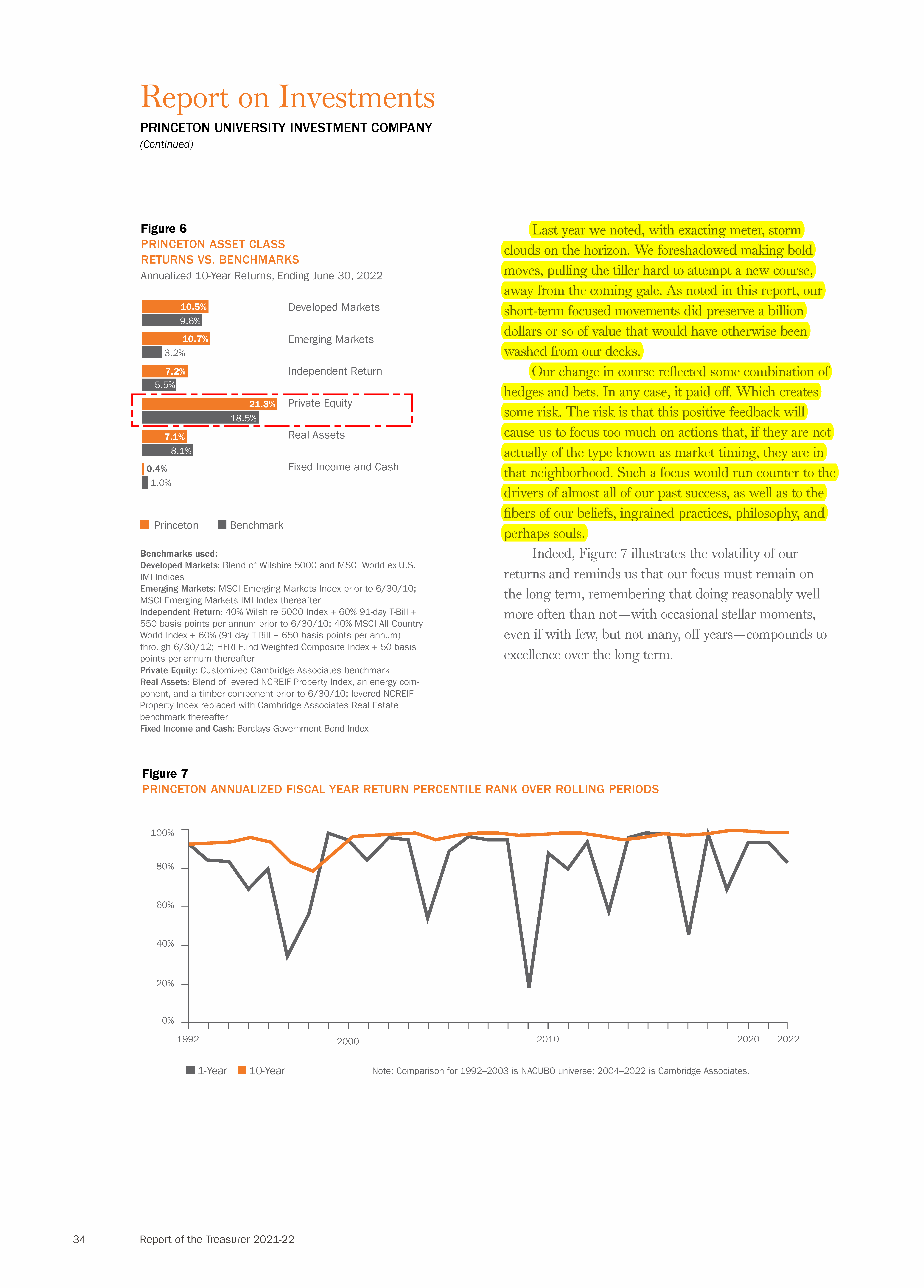

“Even with the significant reduction in the Private Equity target, Princo still continued to recognize a large overweight in Private Equity, which is unintentional and is due to two key factors. Firstly, with the benefit of hindsight, we recognize that our commitments to Private Equity funds during fiscal years 2006 through 2008 were too high. Since that time, we have reduced our commitment pace to a sustainable steady-state rate and expect to glide gradually over multiple years back to the target allocation. Indeed, this decline would be happening at a faster pace if not for the second factor—the asset category’s very strong performance. Private Equity has generated a 27.7 percent annualized return over the past five years relative to a 5.7 percent annualized return for the Endowment excluding Private Equity. Over the past two fiscal years, we have received significant net cash flow from Private Equity investments. Looking ahead, we are cautiously optimistic that the Private Equity portfolio will continue to generate meaningful liquidity in the next several years. It will, however, take substantial time for exposure to decline to the Policy target level.”

“Last year we noted, with exacting meter, storm clouds on the horizon. We foreshadowed making bold moves, pulling the tiller hard to attempt a new course, away from the coming gale. As noted in this report, our short-term focused movements did preserve a billion dollars or so of value that would have otherwise been washed from our decks.

Our change in course reflected some combination of hedges and bets. In any case, it paid off. Which creates some risk. The risk is that this positive feedback will cause us to focus too much on actions that, if they are not actually of the type known as market timing, they are in that neighborhood. Such a focus would run counter to the drivers of almost all of our past success, as well as to the fibers of our beliefs, ingrained practices, philosophy, and perhaps souls.”

Source:

Princeton Office of Finance and Treasury - Report of the Treasurer 2022

As markets fluctuate, Princeton endowment supports almost every aspect of the University

University endowment generates first loss since Great Recession in 2008

Tweets and Posts:

Qubits are insights that we find and share with you.