Qubit: Research on Startup Board Control

Qubit: Research on Startup Board Control

Founders, it cannot be overemphasized how important it is who you add to your board as the company grows. Cause when times get rough, they might fire you.

Something to keep in mind as you raise more money from more investors.

“One decision that involves a clear conflict between these two parties is about whether to replace the founder, and the ex-ante likelihood of such a conflict is higher if the VC has a reputation for replacing founders in the past. We therefore identify VC investors with a particularly high propensity of replacing the CEO in their past portfolio firms. Consistent with the mediation hypothesis, we show that if the first financing round involves at least one such VC, there is a 19% higher likelihood of an independent director being on the board in this round and having a tie-breaking role. These results highlight that unlike in public firms, where independent directors are added to protect investors from the opportunistic behavior of executives (monitoring), independent directors on startup boards are added to protect both, executives and investors, from the opportunistic behavior of the other party (mediation).”

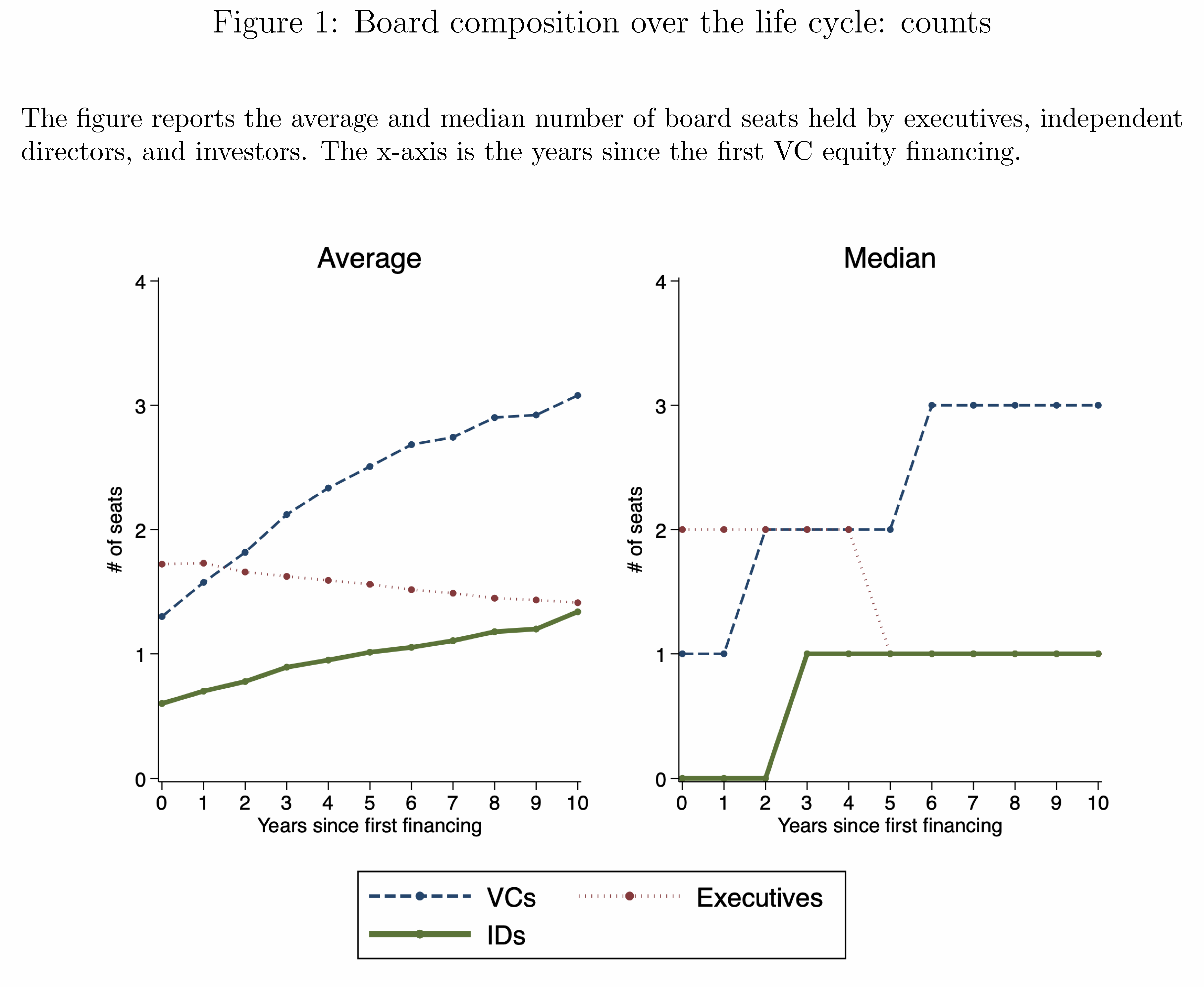

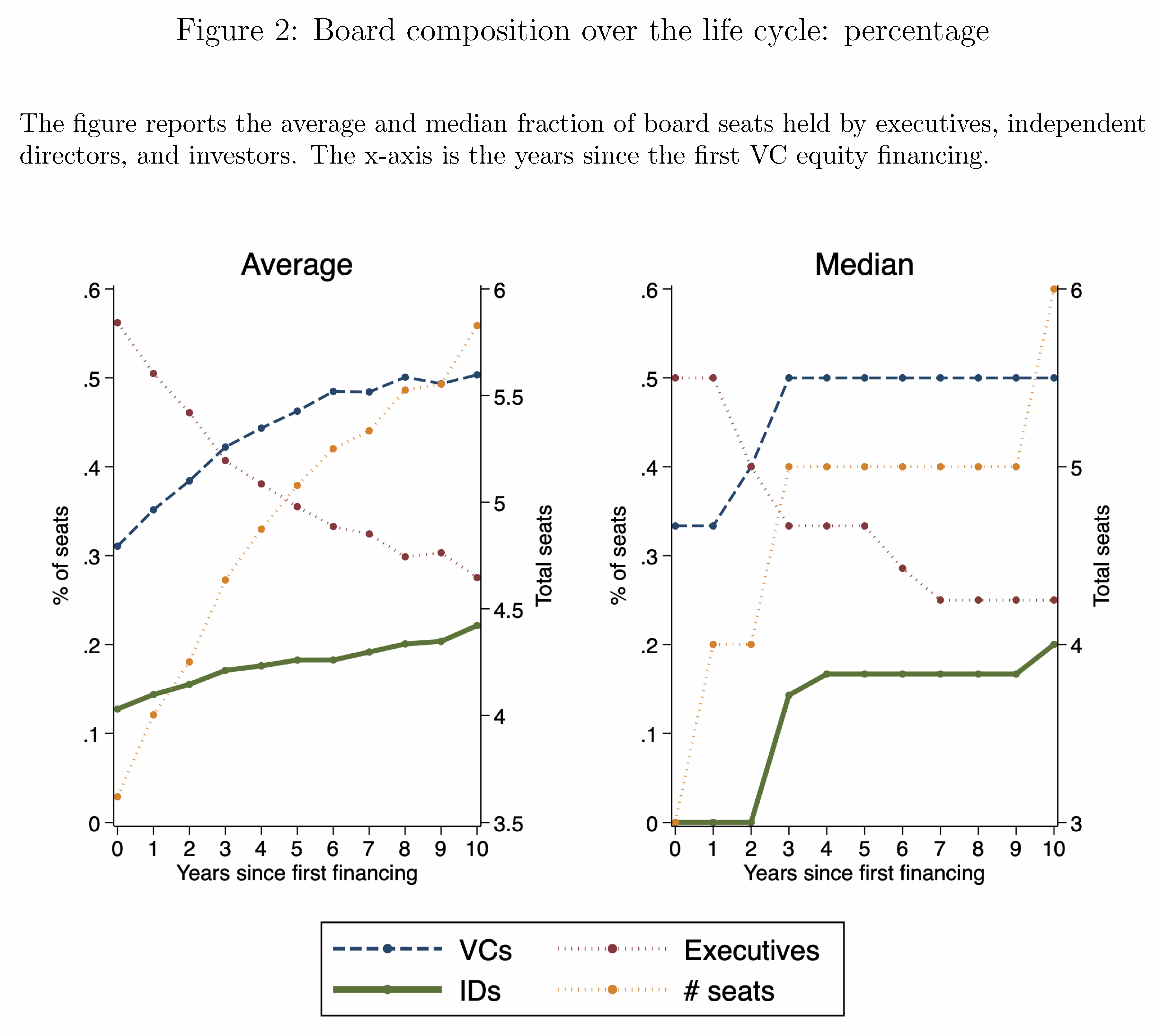

“In the first round, entrepreneurs control about 56% of seats in an average board, and the median board has two entrepreneurs and one VC director. In the second round, the firm adds another VC director, but simultaneously also adds an independent director. The most common arrangement is thus shared control: the median board has two entrepreneurs, two investors, and one independent director to break the tie in case of disagreement, and the average percentages of entrepreneur and VC board seats are 43% and 41% respectively. Over subsequent rounds of financing, the number and fraction of VC directors gradually increase, and by the fourth financing round, the average firm has 53% of board seats controlled by investors.”

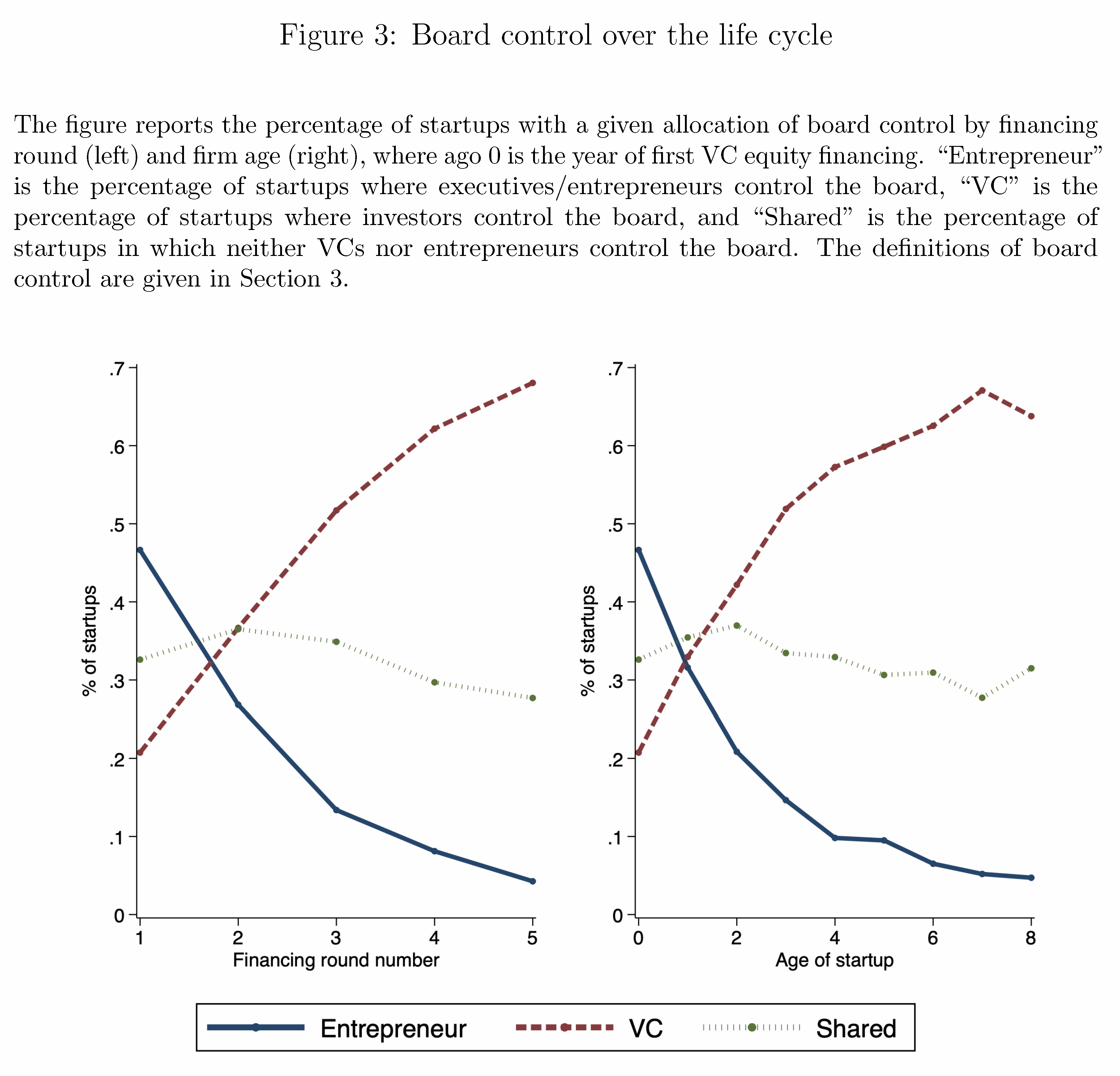

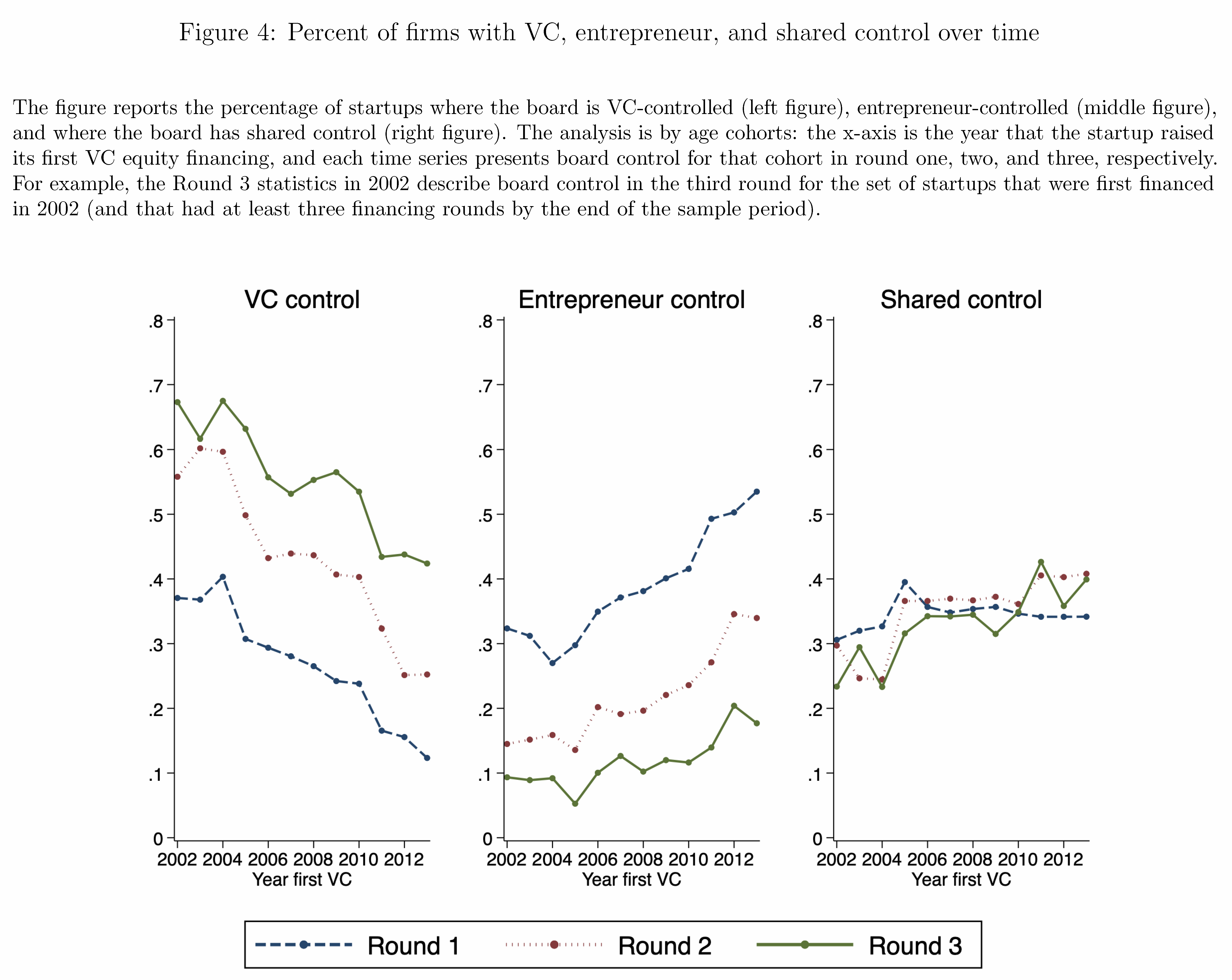

“First, over the firm's life cycle, entrepreneurs lose control over the board, and VC investors gain control. Second, independent directors are playing a key role in this transition, with shared control being particularly common in the second financing round. Moreover, an independent director is typically added together with a new VC director, as if to prevent a deadlock situation or a switch of control to VCs that would have occurred otherwise. Finally, over the last decades, control has shifted from VCs to entrepreneurs, but the role of independent directors has remained important.”

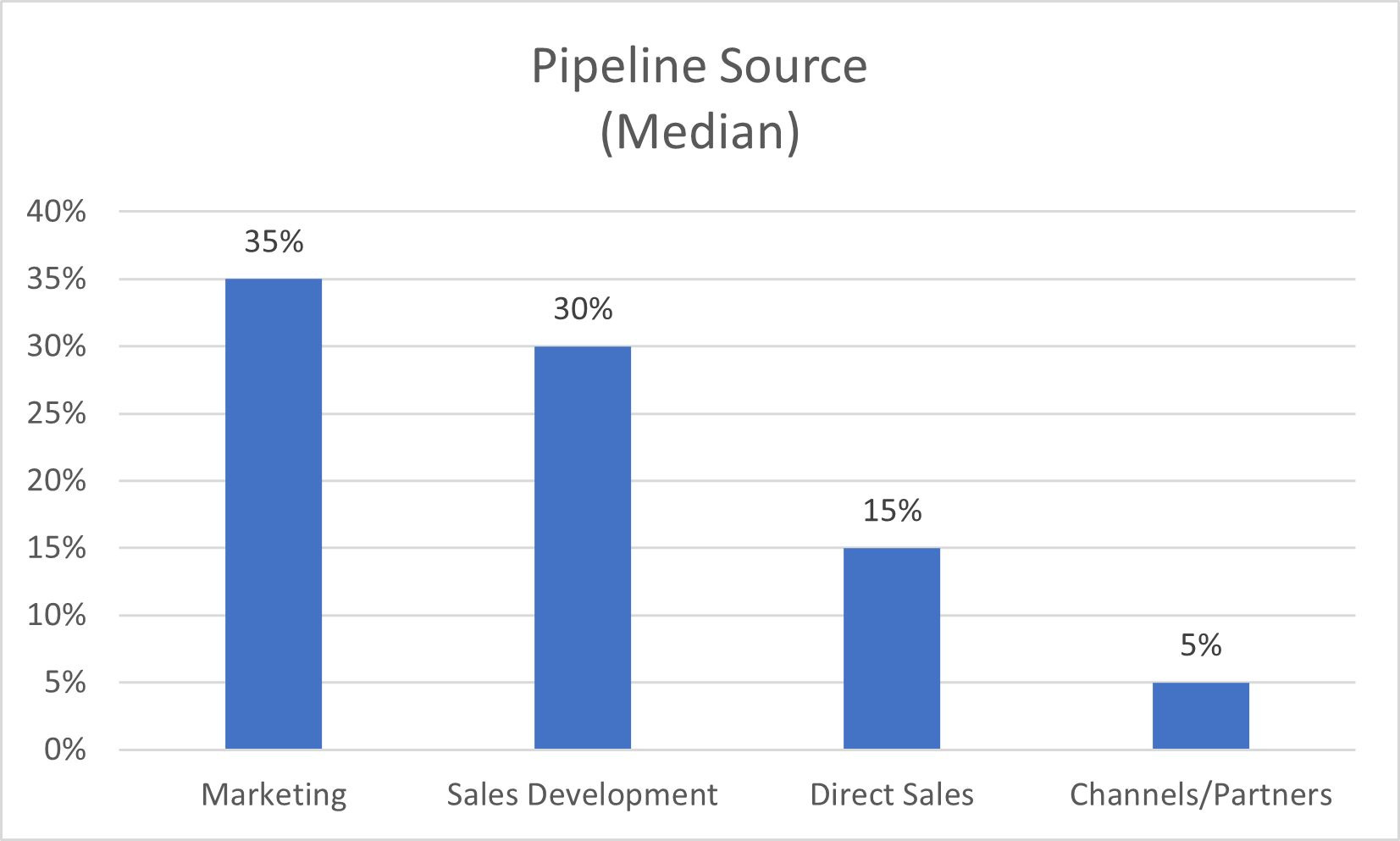

Source:

Board Dynamics Over the Startup Life Cycle

Tweets and Posts:

Qubits are insights that we find and share with you.