Qubit: Research on US Unicorns

Qubit: Research on US Unicorns

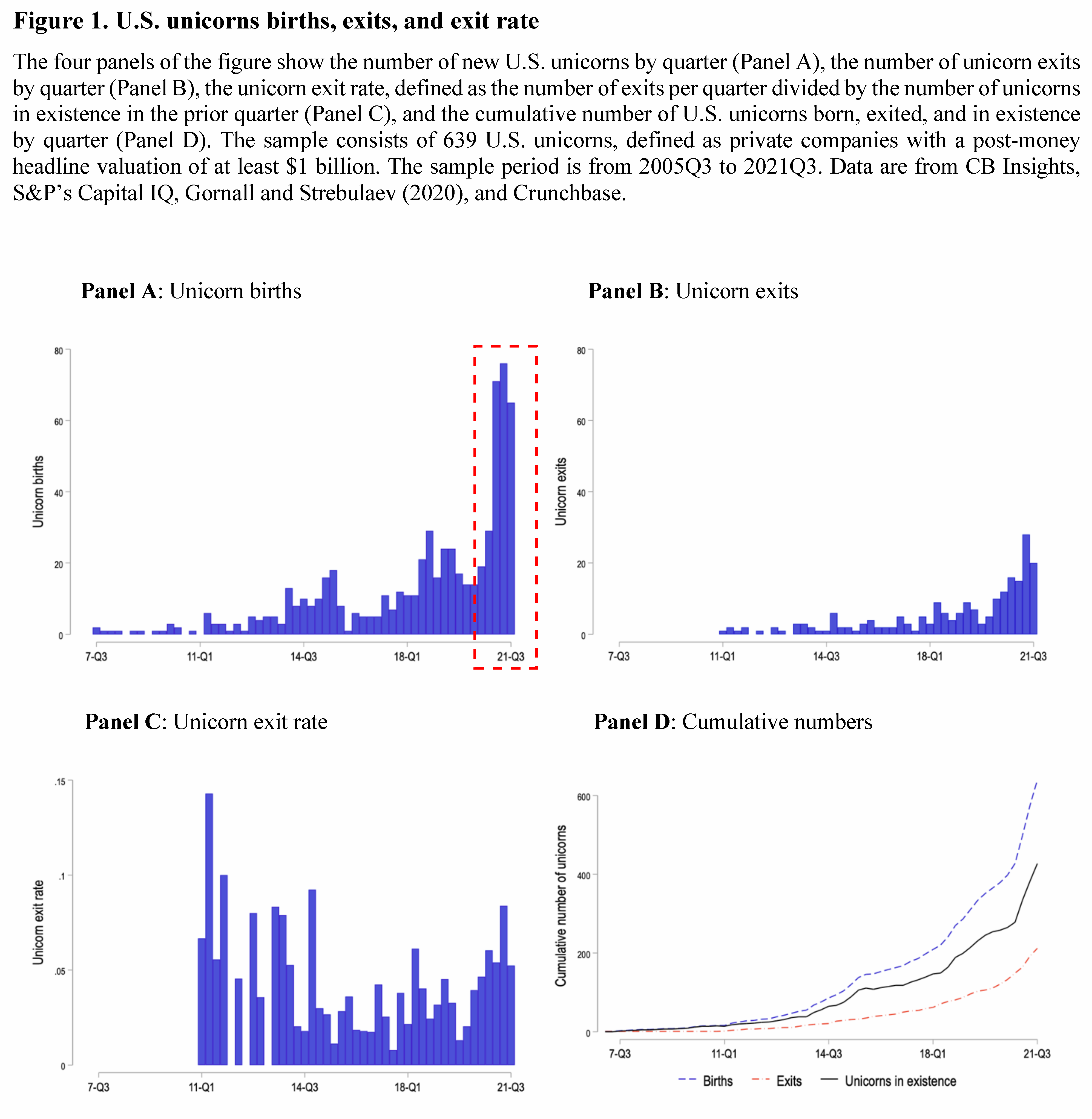

Since 2010, 639 startups based in the U.S. became unicorns.

The average company:

Took 6.9 years to become unicorns

Took 5.3 rounds of equity financing before becoming unicorns

Raised $328 million before becoming unicorns

Raised $708 million total as private companies

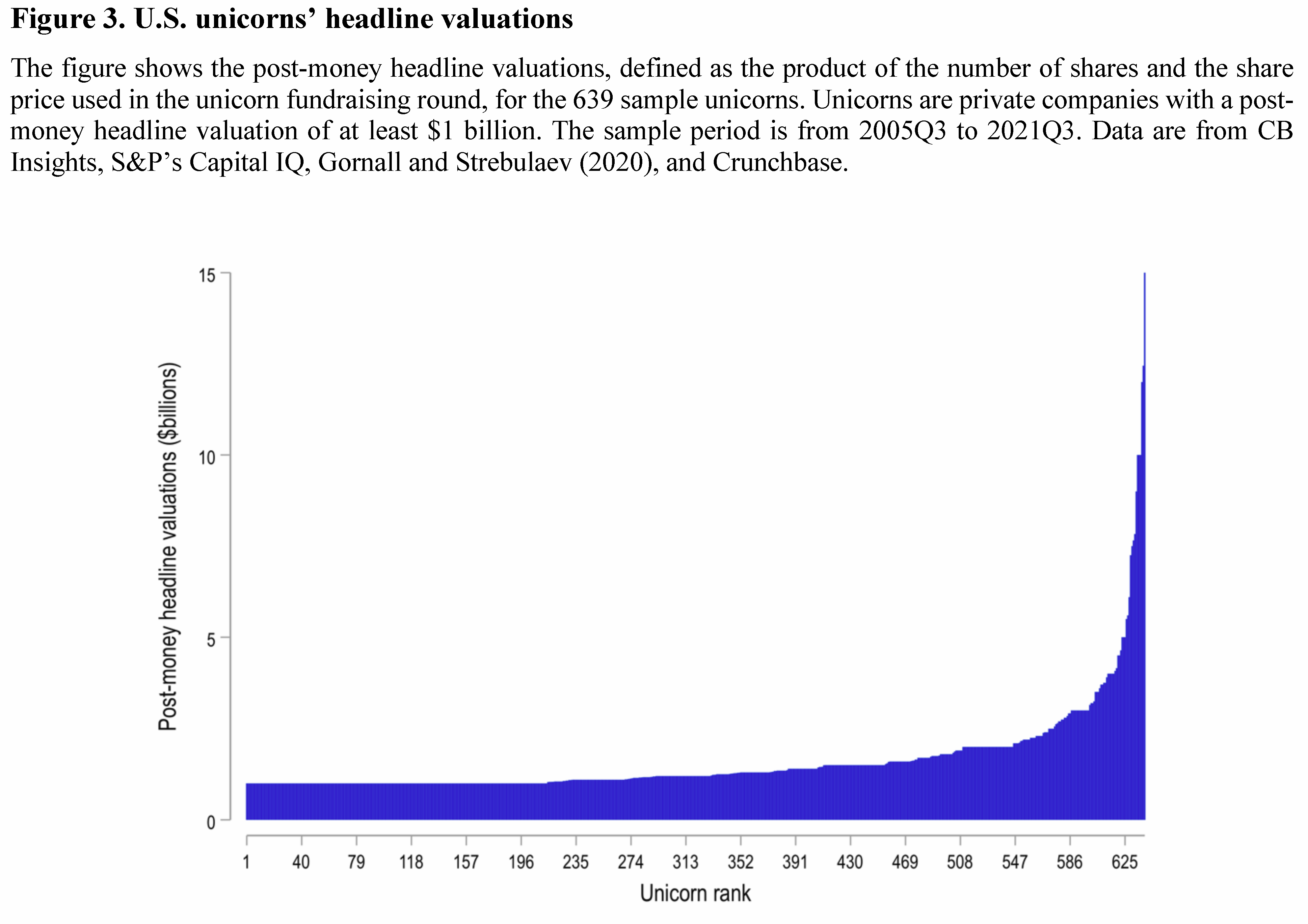

Average post-money headline valuation of the unicorn round was $1.64 billion

Average post-money headline valuation of last financing round was $4.07 billion

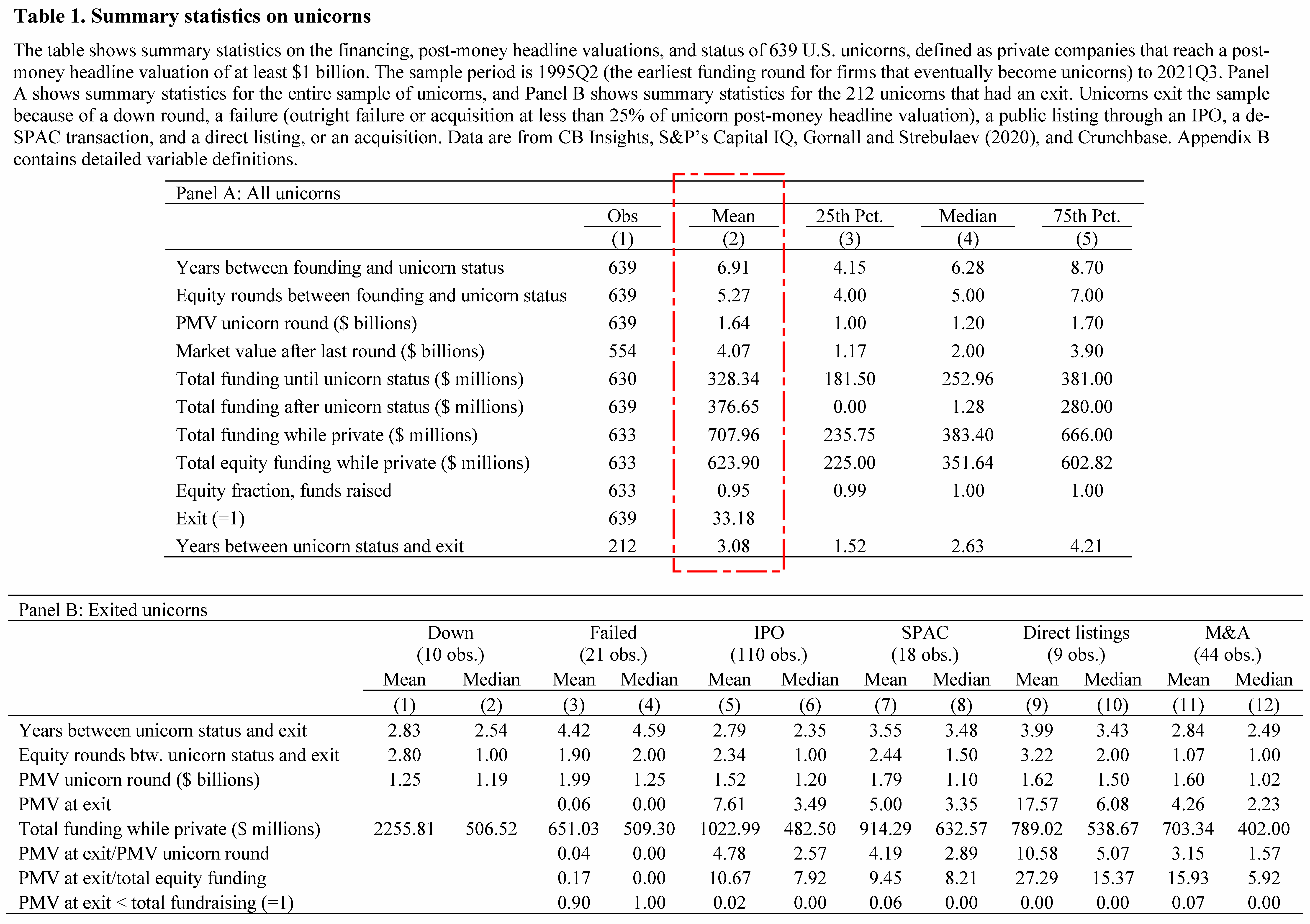

“The average firm took 6.9 years to reach unicorn status (median 6.3). The mean firm became a unicorn after 5.3 rounds of equity financing (median 5 rounds). The average post-money headline valuation of the unicorn round was $1.64 billion, and the median was $1.2 billion. The average post-money headline valuation of the last financing round (be it a private round or the exit valuation) was $4.07 billion (median $2.0 billion).

Unicorns raised on average $328 million in funding until they became unicorns, and a total of $708 million as a private company (medians are $253 and $383 million, respectively). Equity rounds were the dominant financing method, with the mean unicorn raising 95% of all funds through equity rounds, and the median unicorn raising 100% through equity financing. We observe exits for 33.17% (or 212 unicorns) of the total sample. For the subset of firms that exit, the time between the unicorn round and exit was slightly more than three years, for a total average life as a private company of 10 years.”

“… on average, a unicorn that IPOs stays private 2.79 years between achieving unicorn status and the IPO and has on average an additional 2.34 equity financing rounds as a private company. The average (median) PMV at exit for an IPO firm is 4.78 (2.57) times the average (median) PMV at the unicorn round. On average (median), the IPO firm raises $1.02 billion ($483 million) of funding before the IPO. Firms that exit through a SPAC are unicorns on average 3.55 years when they exit, after 2.4 additional equity financing rounds as a private company. They raise on average (median) $914 million ($633 million). Their average (median) PMV at exit is 4.19 (2.89) the PMV at the unicorn round. The direct listing firms were on average unicorns for 4 years and raised an additional 3.22 equity financing rounds as private companies. They raise amounts comparable to the firms that exit through IPOs or SPACs. However, they have a much higher PMV at exit relative to the PMV at the unicorn round since it is 10.6 on average and 5.07 at the median. The last exit category is exit through an acquisition. The number of acquired unicorns is small at 44. The acquired unicorns have been unicorns for a similar number of years compared to those that exit through an IPO but had on average fewer additional equity financing rounds (1.07). The PMV at exit for the acquired unicorns relative to the PMV at the unicorn round is smaller than that of IPOs. The average is 3.2 compared to 4.8, and the median is 1.57 compared to 2.57.”

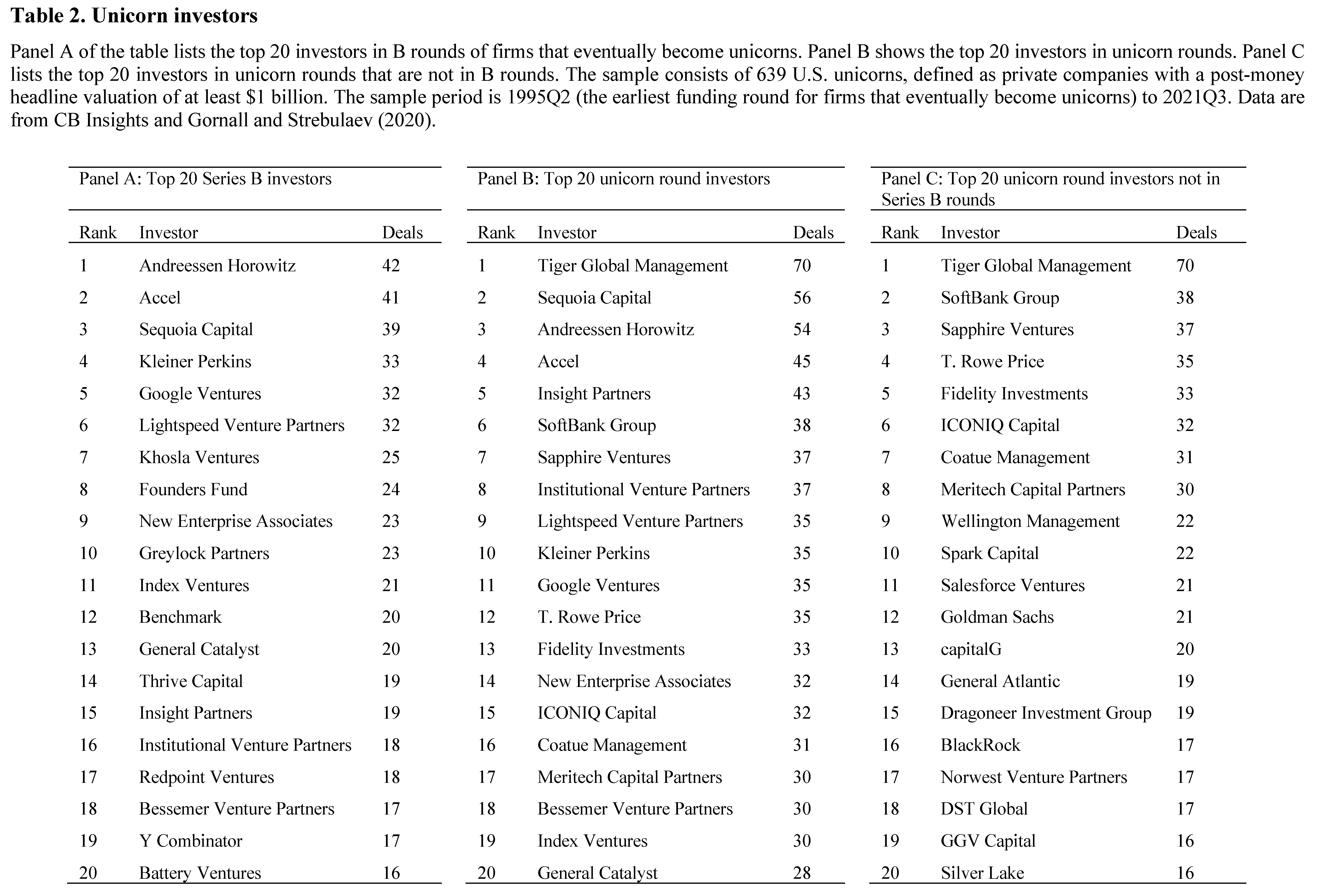

“The top investors that show up in unicorn rounds but not in B rounds are a mix of different types of investors. As expected, four mutual fund complexes, BlackRock, Fidelity, T. Rowe Price, and Wellington Management are active investors in unicorn rounds. However, the top investor is Tiger Global Management, an investment management firm with both public and private equity investment strategies. Though it invests in private businesses of all stages, its investment style makes it better suited to invest in more advanced rounds. Other investment firms in the list are growth-stage private equity investors. For instance, Meritech describes its objective to ‘invest in the best late-stage tech companies in the universe.’ One of the most active investors in unicorn rounds is ICONIQ Capital, which is part family office to some billionaires (for instance, Mark Zuckerberg) and part private equity and venture capital general manager. Many of these investors that show up at the unicorn round are known for having a different degree of involvement in the companies in which they invest and different due diligence requirements than investors who participate in earlier rounds. For instance, they are unlikely to want board seats. Chernenko, Lerner, and Zeng (2021) show how rights granted to mutual fund companies typically differ from those granted to venture capital funds.”

Source:

Tweets and Posts:

Qubits are insights that we find and share with you.