Qubit: Research on VC Contracting

Qubit: Research on VC Contracting

When negotiating a term sheet with VCs, the two things that matter most as a founder are: economics and control.

But only a small number of you will be an outstanding venture outcome.

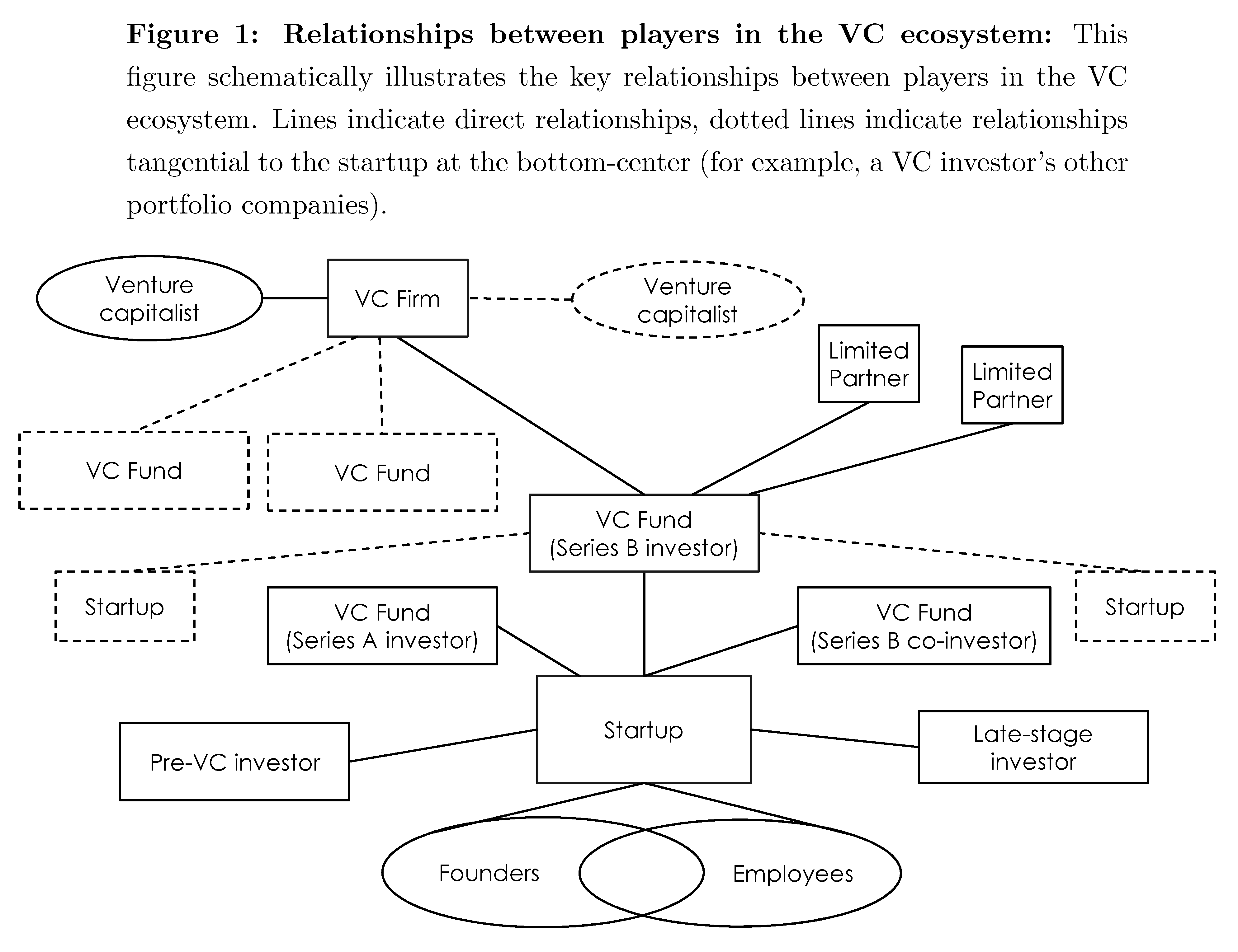

This paper by Professors Will Gornall and Ilya Strebulaev provides a detailed overview on how venture rounds of financing work for startups.

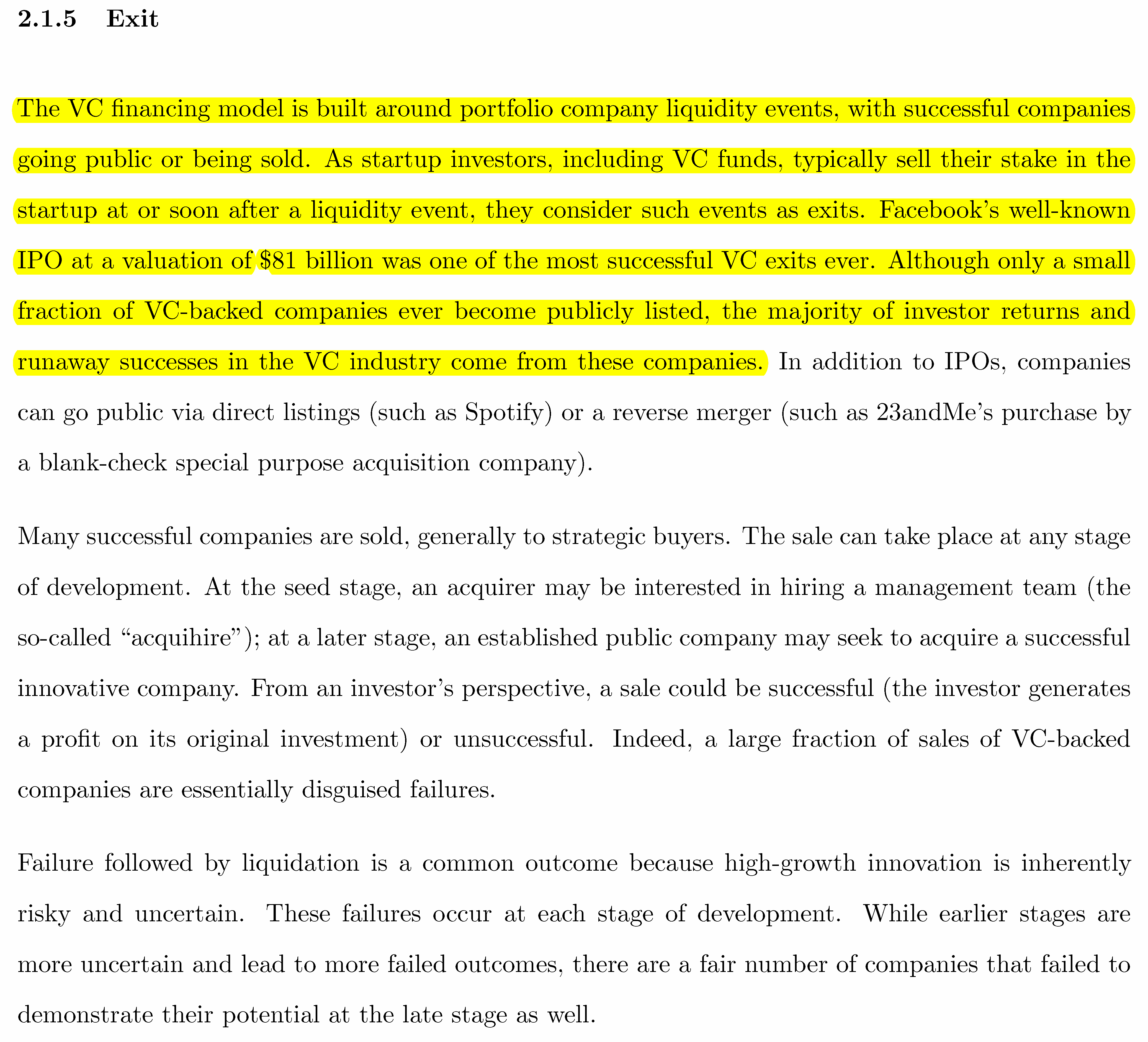

“The VC financing model is built around portfolio company liquidity events, with successful companies going public or being sold. As startup investors, including VC funds, typically sell their stake in the startup at or soon after a liquidity event, they consider such events as exits. Facebook’s well-known IPO at a valuation of $81 billion was one of the most successful VC exits ever. Although only a small fraction of VC-backed companies ever become publicly listed, the majority of investor returns and runaway successes in the VC industry come from these companies.”

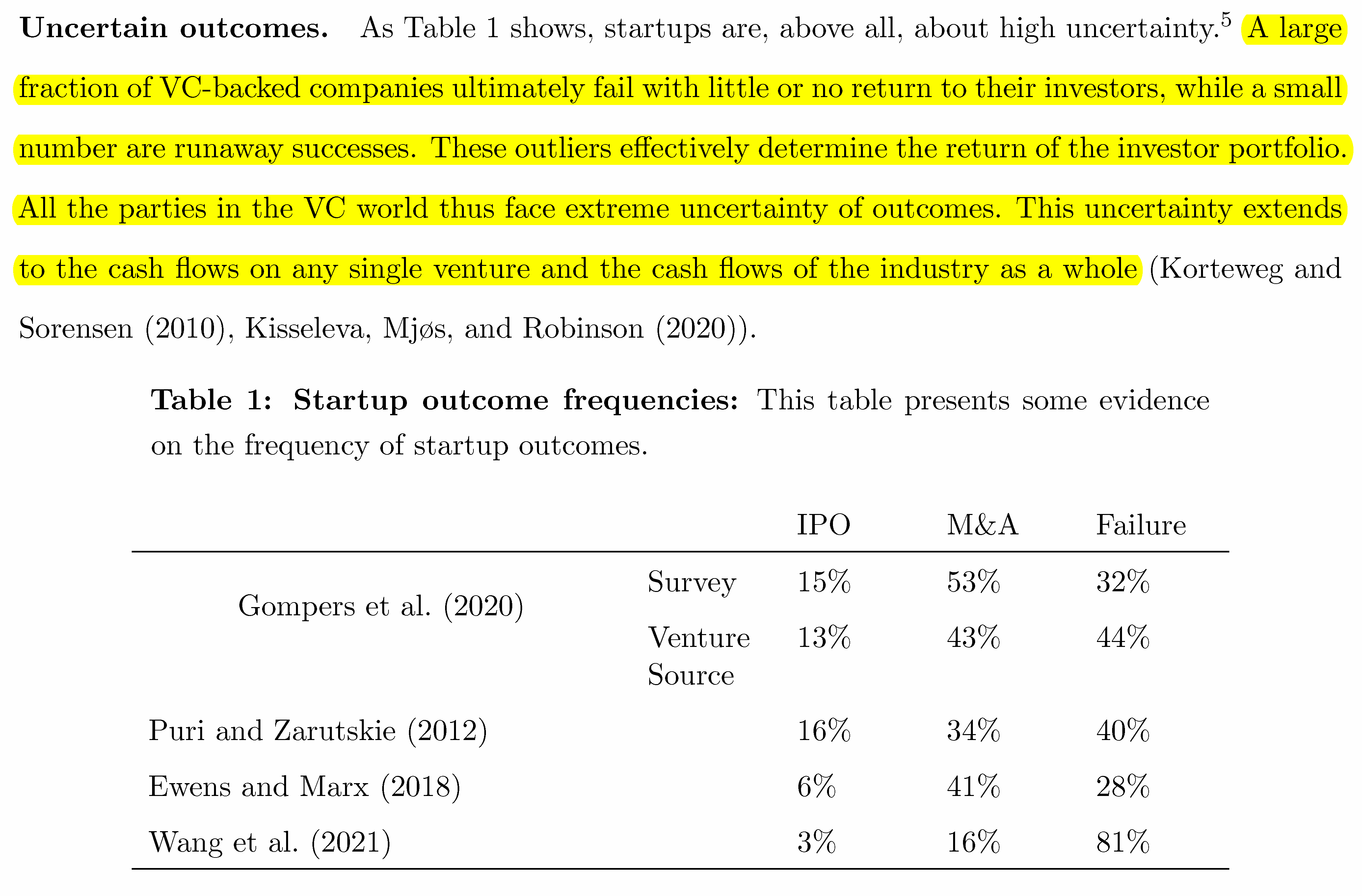

“A large fraction of VC-backed companies ultimately fail with little or no return to their investors, while a small number are runaway successes. These outliers effectively determine the return of the investor portfolio. All the parties in the VC world thus face extreme uncertainty of outcomes. This uncertainty extends to the cash flows on any single venture and the cash flows of the industry as a whole.”

“The challenges of valuing (especially very) early-stage startups mean that valuation is triangulated from applying judgment-based rules. For example, based on their experience VCs may have a specific target ownership stake on a fully diluted basis. The minimum investor ownership stake may be viewed by investors as necessary to maintain control rights in light of expected future dilution and is often determined by the economic considerations of VC funds rather than a specific startup. The ceiling on the target ownership stake is designed to preserve founder-manager incentives and ensure interest on behalf of future investors. In the very first VC rounds, the ownership stake has historically been within the range between 15% and 30%. In addition, while the expected future cash flows are difficult to estimate, investors can forecast expenses (and thus the amount they need to invest) for the relatively short period of time (typically until the next investment round, that is, over a 12- to 18-month horizon) with much better precision.”

Source:

The Contracting and Valuation of Venture Capital-Backed Companies

Tweets and Posts:

Qubits are insights that we find and share with you.