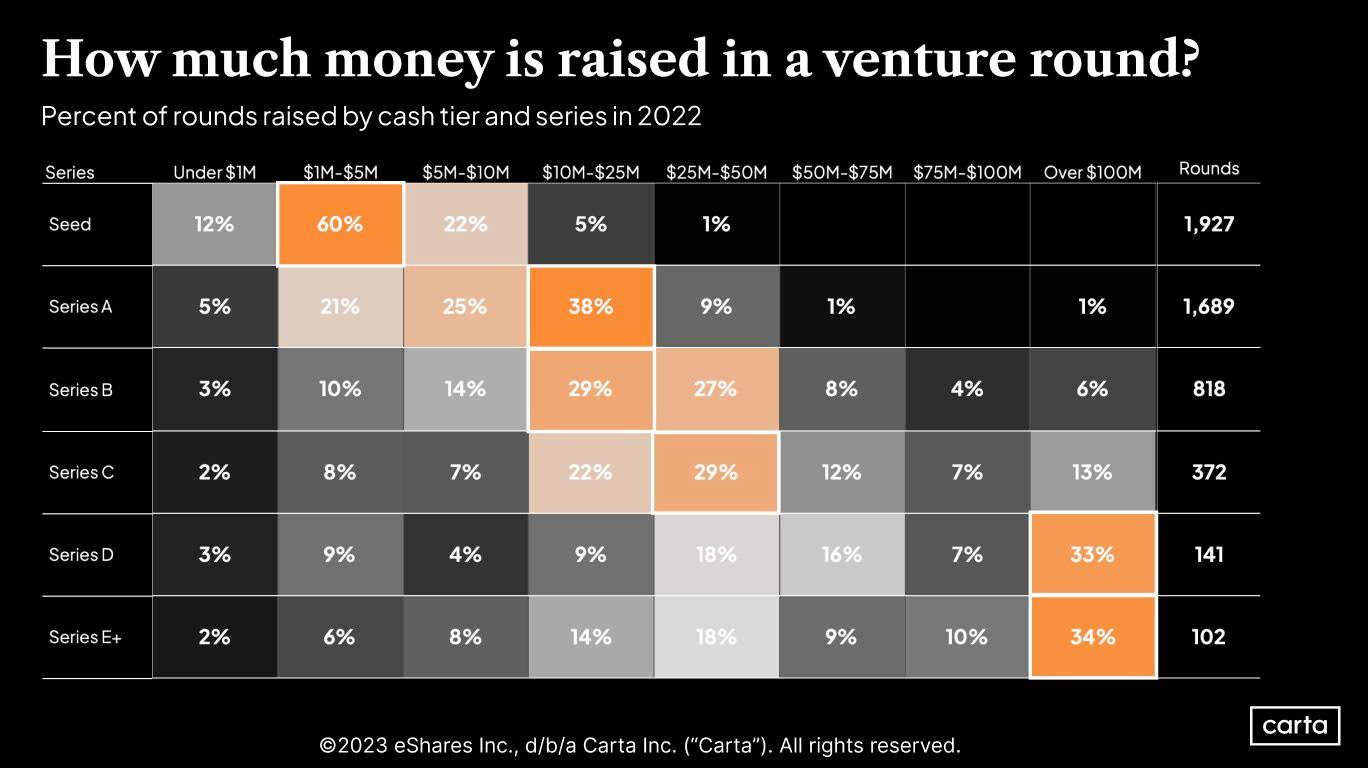

Qubit: Research on VC Decisions

Qubit: Research on VC Decisions

According to this VC survey that was published back in 2016:

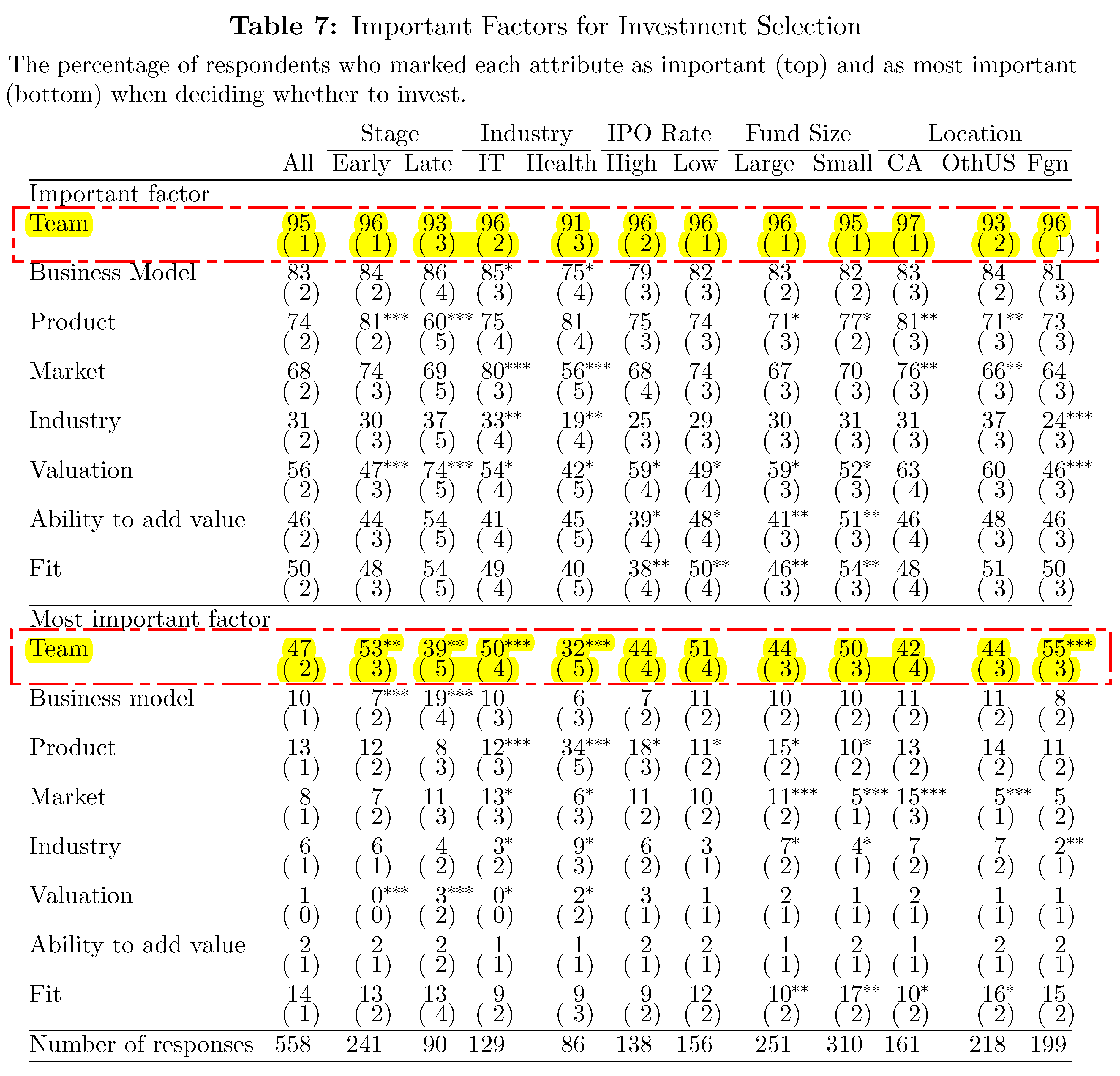

Founding team is the most important factor to startup success (or failure)

Team selection is the most important factor to creating value

Deal flow, deal selection, and post-investment value-add help generate returns, but deal selection is considered the most important

Median VC firm closes on 4 deals per year

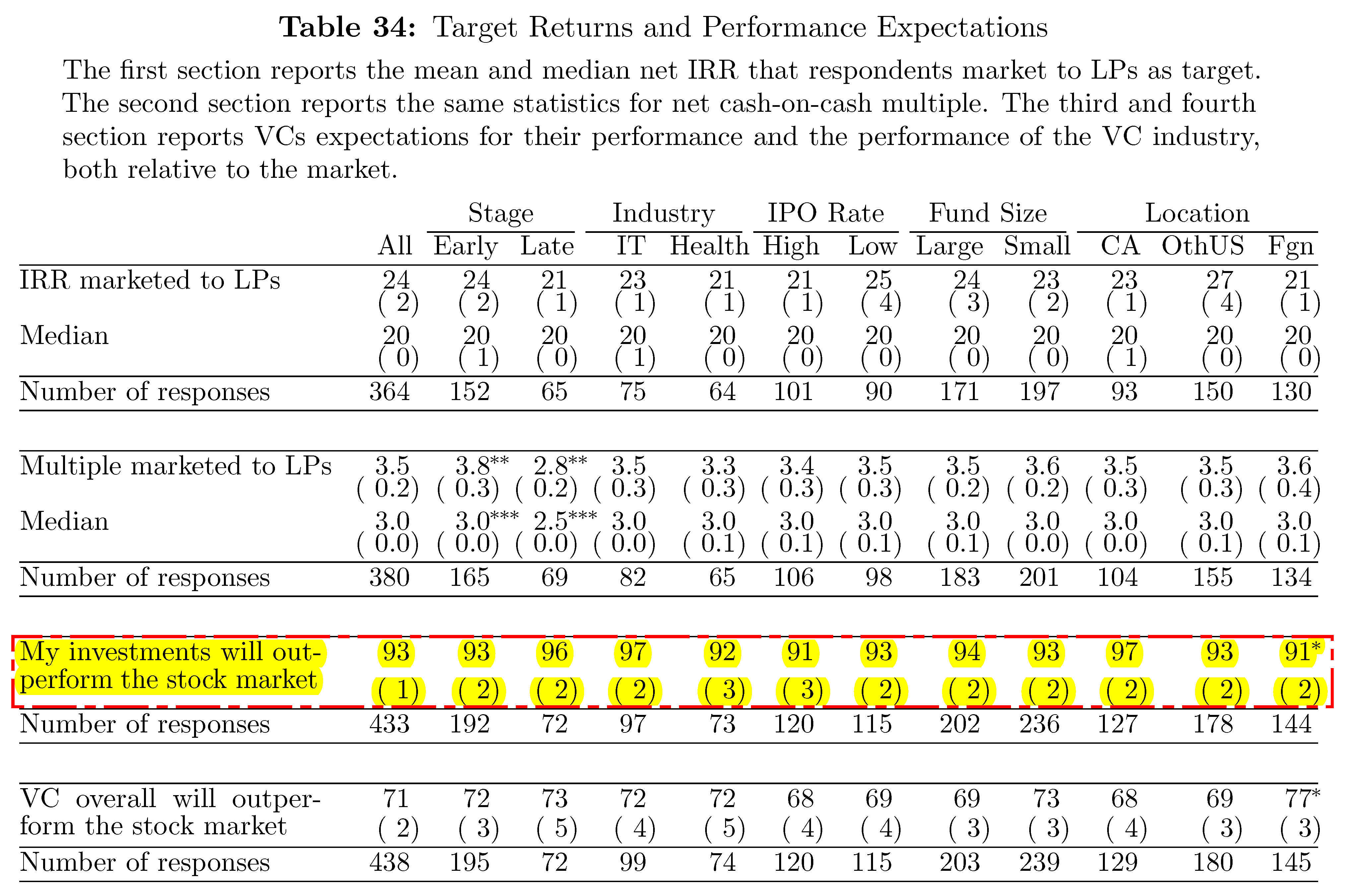

Average required IRR is 31%, average cash-on-cash multiples is 5.5

What's remarkable is that 93% of VCs surveyed expect to beat the market on a relative basis.

This is a classic example of the Lake Wobegon effect.

“When asked which of their activities—deal flow, deal selection or post-investment value-added—helped generate their returns, a majority of VCs reported that each of the three contributed with deal selection being the most important of the three. Deal selection was ranked as important by 86% of VCs and as most important by 49% of VCs. Post-investment value-added was seen as important by 84% of VCs and as most important by 27% of VCs. Deal flow was ranked as important by 65% and as most important by 23%. These results are consistent with the estimates in Sorensen (2007) that deal flow and deal selection are more important than value-add, but all three are important. These results, however, extend and inform Sorensen (2007) by distinguishing between deal flow and deal selection.

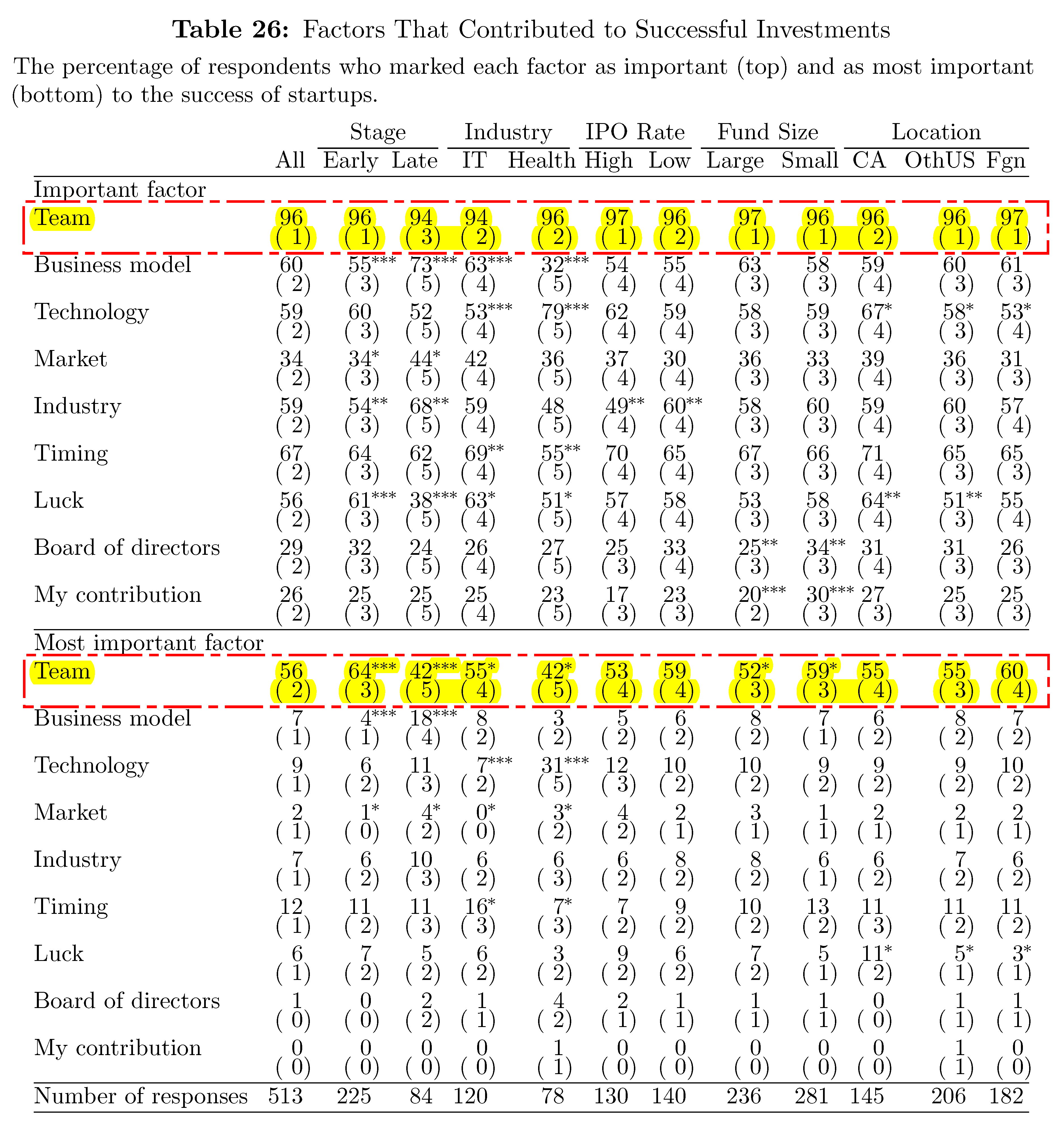

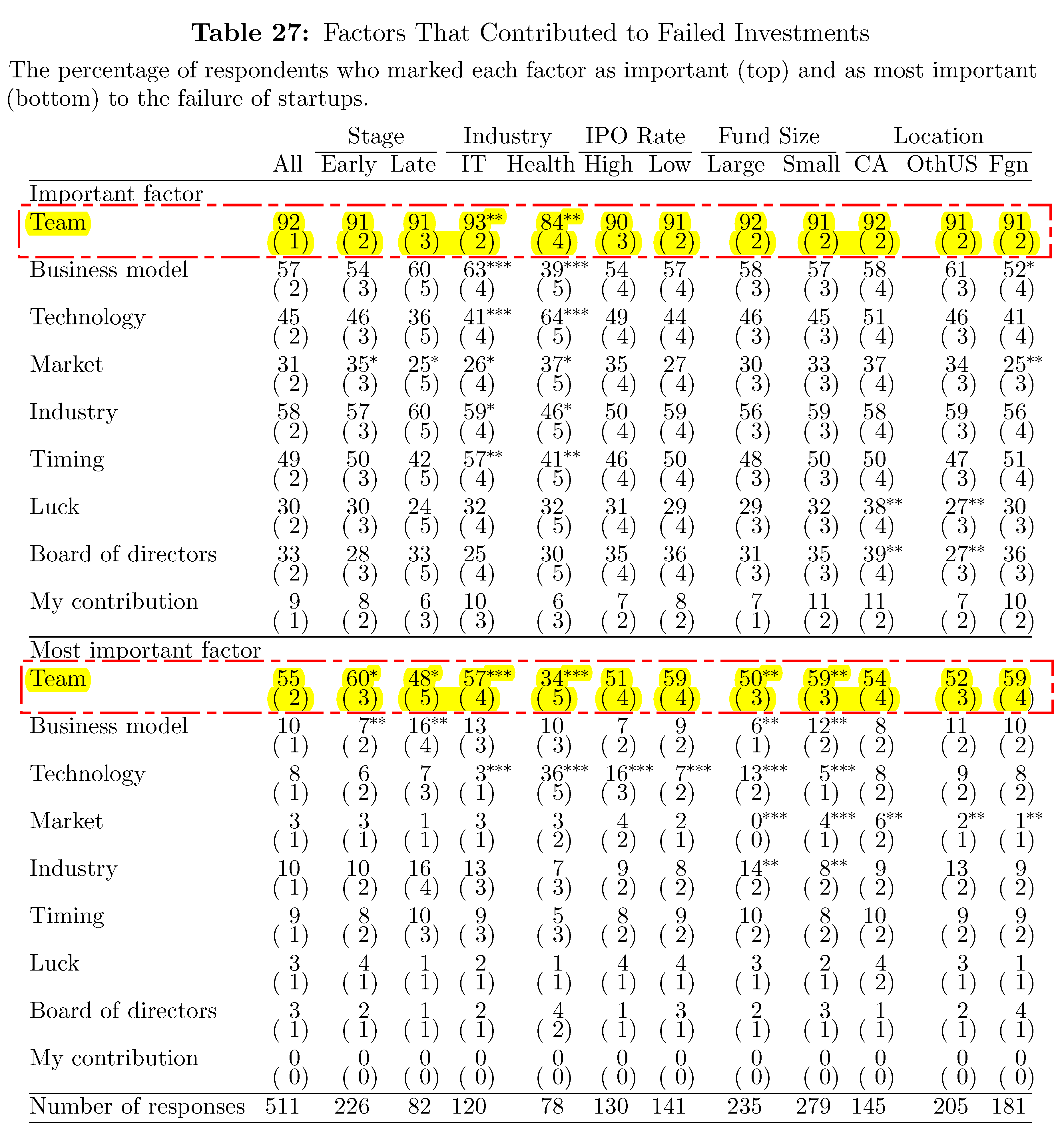

We also asked VCs what factors contributed most to their successes and failures. Again, the team was by far the most important factor identified, both for successes (96% of respondents) and failures (92%). For successes, each of timing, luck, technology, business model, and industry were of roughly equal importance (56% to 67%). For failures, each of industry, business model, technology and timing were of roughly equal importance (45% to 58%). Perhaps surprisingly, VCs did not cite their own contributions as a source of success or failure.”

“The median firm closes about 4 deals per year. The table shows that for each deal in which a VC firm eventually invests or closes, the firm considers roughly 100 potential opportunities. At each subsequent stage a substantial number of opportunities are eliminated. One in four opportunities lead to meeting the management; one-third of those are reviewed at a partners meeting. Roughly half of those opportunities reviewed at a partners meeting proceed onward to the due diligence stage. Conditional on reaching the due diligence stage, startups are offered a term sheet in about a third of cases. Offering a term sheet does not always result in a closed deal, as other VC firms can offer competing term sheets at the same time. Similarly, legal documentation and representations/warranties may cause deals to fall apart between agreeing to a term sheet and the deal closing. The fact that VC firms on average offer 1.7 term sheets for each deal that they close, a close rate of roughly 60%, suggests that a meaningful number of opportunities that ultimately receive funding are not proprietary.”

“The average required IRR is 31%, which is higher than the 20 to 25% IRR reported by private equity investors in Gompers et al. (forthcoming). Late-stage and larger VCs require lower IRRs of 28% to 29% while smaller and early-stage VCs have higher IRR requirements. The same pattern holds in cash-on-cash multiples, with an average multiple of 5.5 and a median of 5 required on average, with higher multiples for early-stage and small funds. The source of these differences is not entirely clear. Early-stage funds may demand higher IRRs due to higher risk of failure, i.e., they may calculate IRRs from ‘if successful’ scenarios. Small funds potentially demand higher IRRs due to capital constraints or the fact that they invest in, on average, earlier stage deals.”

Source:

How Do Venture Capitalists Make Decisions?

Harvard Law School Forum on Corporate Governance: How Do Venture Capitalists Make Decisions?

Tweets and Posts:

Qubits are insights that we find and share with you.