Qubit: SVB Market Report H1 2023

Qubit: SVB Market Report H1 2023

Startups today are much more sophisticated than past cohorts and yet they face the same problems when capital dries up and the focus on growth at all costs suddenly shifts to profitability.

Latest IPO companies had 6x median revenue and 3x more operating experience than dot-com companies

Median Series A company growing into its valuation is 3 months, for median late-stage company is 13 months

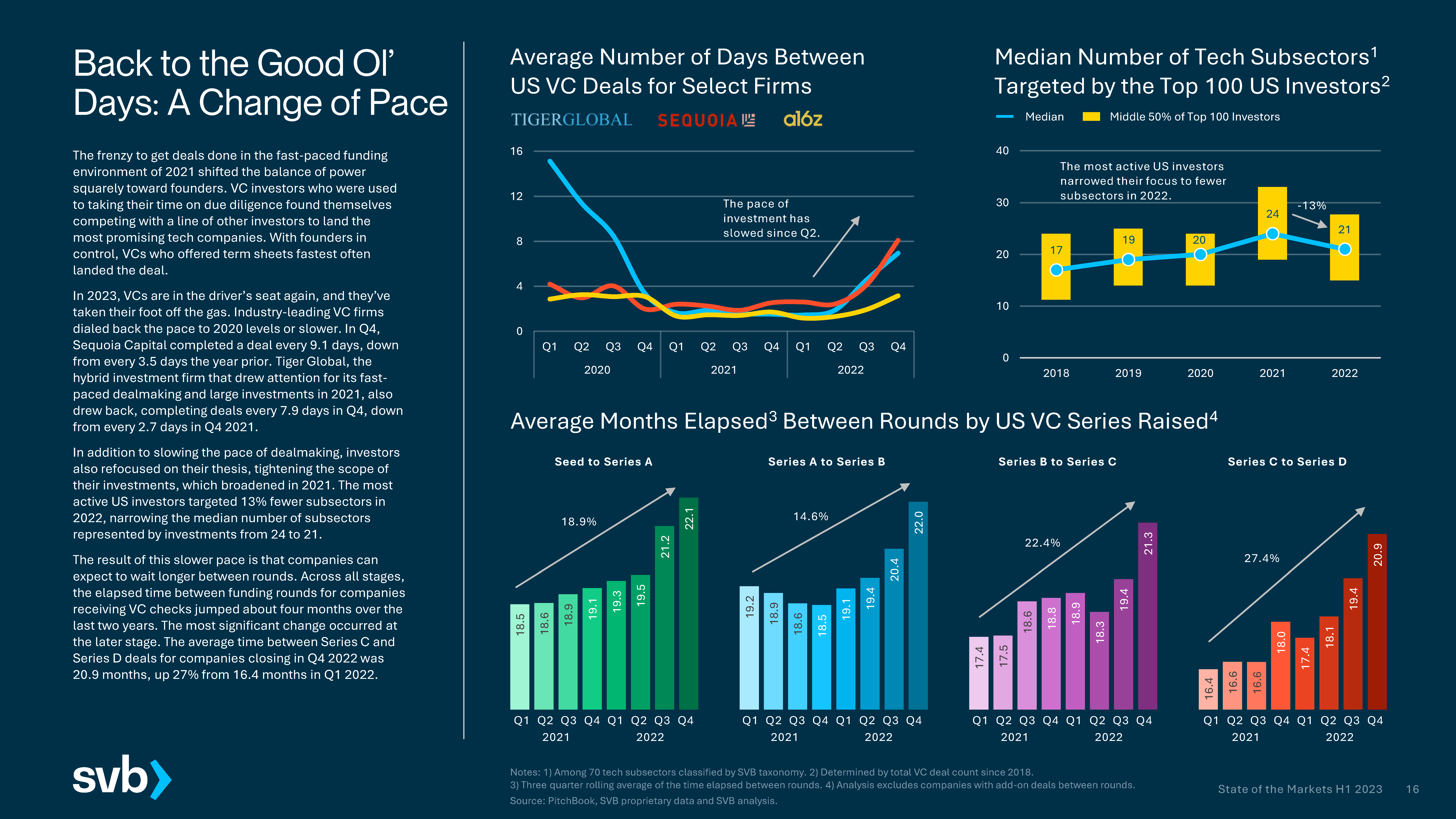

Elapsed time between funding rounds jumped about 4 months over the last couple of years

Median cash runway has fallen from 16 months a year ago to barely 12 months now

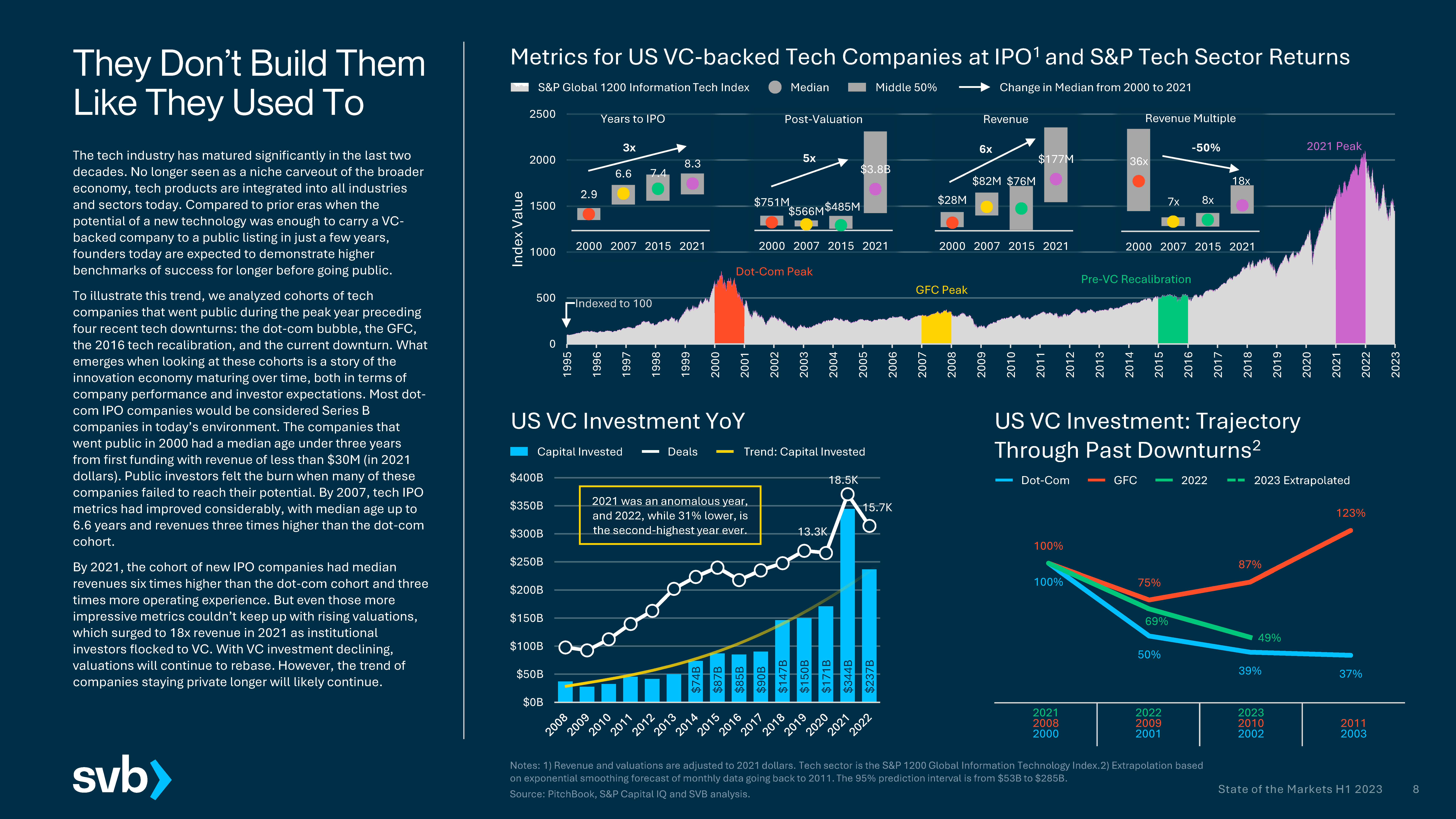

“The tech industry has matured significantly in the last two decades. No longer seen as a niche carveout of the broader economy, tech products are integrated into all industries and sectors today. Compared to prior eras when the potential of a new technology was enough to carry a VC-backed company to a public listing in just a few years, founders today are expected to demonstrate higher benchmarks of success for longer before going public.

To illustrate this trend, we analyzed cohorts of tech companies that went public during the peak year preceding four recent tech downturns: the dot-com bubble, the GFC, the 2016 tech recalibration, and the current downturn. What emerges when looking at these cohorts is a story of the innovation economy maturing over time, both in terms of company performance and investor expectations. Most dot-com IPO companies would be considered Series B companies in today’s environment. The companies that went public in 2000 had a median age under three years from first funding with revenue of less than $30M (in 2021 dollars). Public investors felt the burn when many of these companies failed to reach their potential. By 2007, tech IPO metrics had improved considerably, with median age up to 6.6 years and revenues three times higher than the dot-com cohort.

By 2021, the cohort of new IPO companies had median revenues six times higher than the dot-com cohort and three times more operating experience. But even those more impressive metrics couldn’t keep up with rising valuations, which surged to 18x revenue in 2021 as institutional investors flocked to VC. With VC investment declining, valuations will continue to rebase. However, the trend of companies staying private longer will likely continue.”

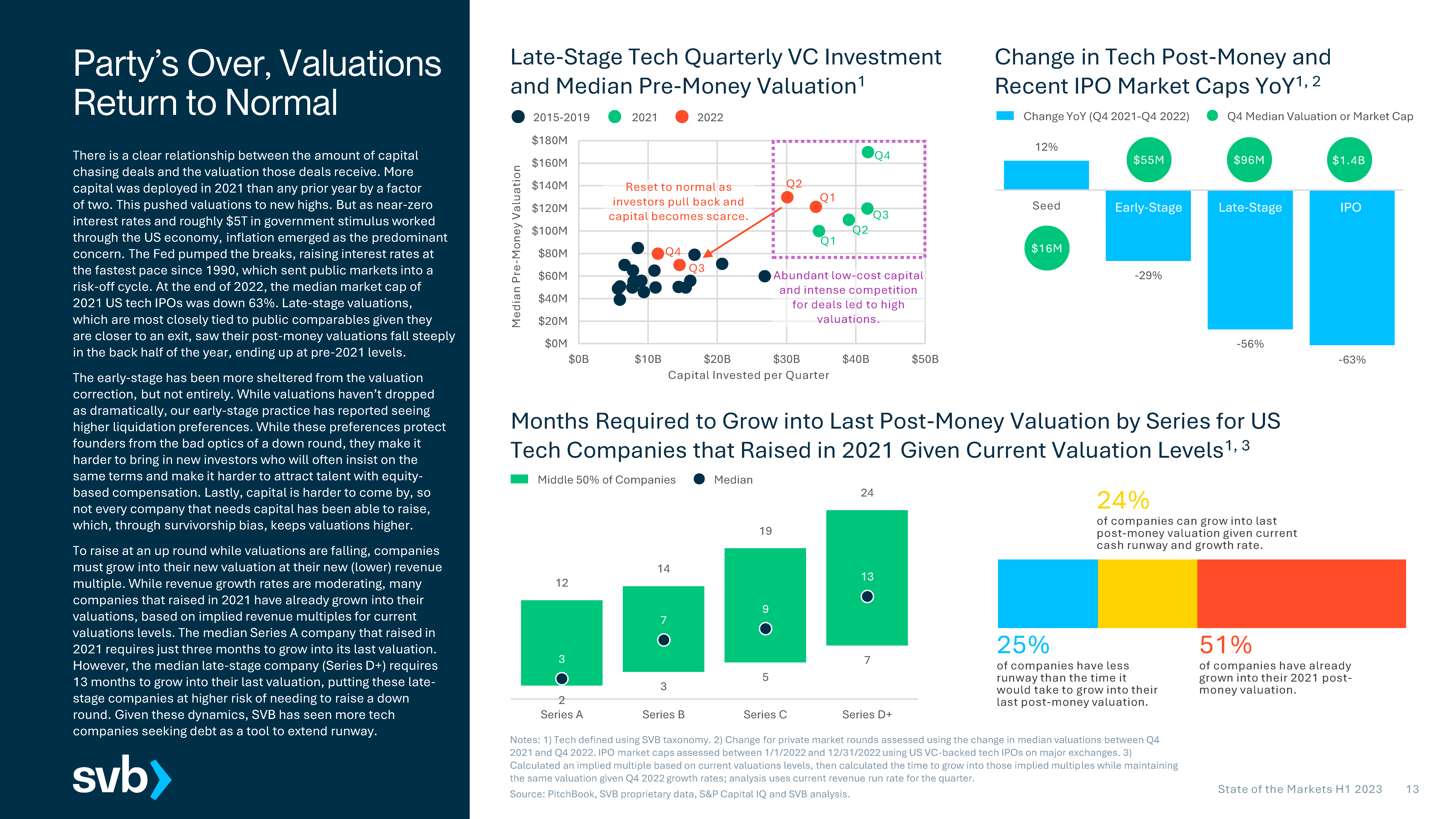

“To raise at an up round while valuations are falling, companies must grow into their new valuation at their new (lower) revenue multiple. While revenue growth rates are moderating, many companies that raised in 2021 have already grown into their valuations, based on implied revenue multiples for current valuations levels. The median Series A company that raised in 2021 requires just three months to grow into its last valuation. However, the median late-stage company (Series D+) requires 13 months to grow into their last valuation, putting these late-stage companies at higher risk of needing to raise a down round. Given these dynamics, SVB has seen more tech companies seeking debt as a tool to extend runway.”

“In 2023, VCs are in the driver’s seat again, and they’ve taken their foot off the gas. Industry-leading VC firms dialed back the pace to 2020 levels or slower. In Q4, Sequoia Capital completed a deal every 9.1 days, down from every 3.5 days the year prior. Tiger Global, the hybrid investment firm that drew attention for its fast-paced dealmaking and large investments in 2021, also drew back, completing deals every 7.9 days in Q4, down from every 2.7 days in Q4 2021.”

“On the other hand, for companies that don’t have ample cash at their disposal, the situation is much more dire. As the market environment remains uncertain, investors have continued to pull back, cutting off critical oxygen for companies to survive. This is ever more important as our proprietary data shows an increasing share of companies with less than 12 months of cash runway. The median cash runway for companies has fallen from 16 months in Q4 2021 to just over 12 months as of Q4 2022. This is just shy of the median length of a recession. However, if this current downturn were to mimic the GFC or 1970s energy crisis — the latter of which has a number of parallels to today’s environment — startups would need closer to 18 to 24 months of runway to survive. Nonetheless, as more companies reach the end of their cash runway, we expect VC activity to increase as companies start to accept lower valuations.”

Source:

State of the Markets - H1 2023 Report

Tweets and Posts:

Qubits are insights that we find and share with you.