Qubit: SVB Market Report H2 2023

2023 is turning out to be the year of the down rounds, layoffs, and lack of liquidity in the world of startups.

Only a quarter of deals in 2023 have disclosed post-money valuations, indicating a higher likelihood of down or flat rounds

Two-thirds of tech layoffs since March 2020 happened in the last 10 months

US VC fundraising dropped 66%, from $102b in H1 2022 to $35b in H1 2023

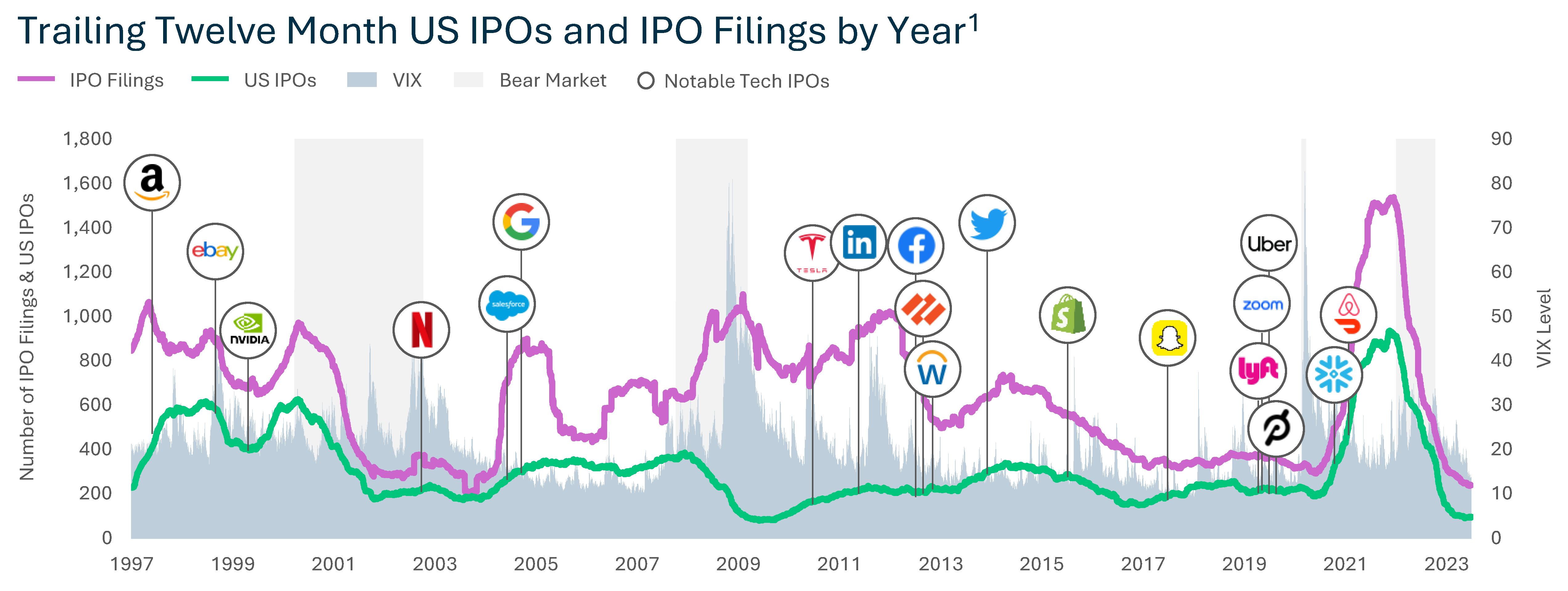

64% of US VC-backed tech IPOs since 2017 are below their IPO market cap, over one-third of those are below their last private valuation

This is not an easy time for a lot of companies.

But for the resilient founder who wants to validate a new idea and build a product behind it, this is a good time as ever to form a startup. Your adaptability, resourcefulness, and tenacity to create something out of nothing will shine through.

There is always capital available for those that work.

“It was only a matter of time. Following a frenzied 2021 dealmaking pace that many deemed unsustainable, the venture slump has hit startups — and finally shown up in the data. This year saw a jump in down rounds, accounting for the largest share of deals since 2018. Down rounds are an unwelcomed event for a number of reasons, namely because they can lead to outsized dilution, disgruntled investors and employees concerned over their equity — not to mention the public black eye.

Even though 2022 was a muted year, startups likely had enough runway due to an exuberant 2021 funding year. As startups have gone back to the venture well this year, they’ve been faced with the harsh reality that yesterday’s price is not today’s price. In fact, Q2 2023 had the highest share of down rounds (12.6%) since Q4 2017 (14.8%). As expected, most of the down rounds are occurring at the late-stage, where public comps are more readily available and the allure of early-stage potential is better understood.

This share of down and flat rounds could be even higher than the data suggests as more companies refuse to disclose their valuation during downturns. This is likely tied to startups wanting to avoid the public scrutiny of raising a down round. Another possible scenario for not disclosing terms is if a company raised less capital or at a lower valuation than initially expected.

Valuation step-ups in 2023 are the lowest they have been post-pandemic. Step-ups have fallen the most at the later stage, with Series C to Series D valuation step-ups decelerating to 22% — the lowest total since 2010. Meanwhile, the earlier stage has remained more resilient as it is less susceptible to changes in the public markets.”

“However, private investors have recently shifted their view on how long they plan to hold portfolio companies that recently had a public exit before selling their position. In fact, nearly one-fifth of 2021 US VC-backed tech IPOs’ outstanding shares are held by private investors — who missed their opportunity to liquidate at market peak and provide distributions to LPs. This puts emphasis on long-term public market performance and a broader economic environment.

As it stands now, it’s likely most private investors will continue to hold on to their recently exited positions, given 64% of US VC-backed tech IPOs since 2017 are below their IPO market cap. Even compared to measures like last private valuation (LPV), over one-third of that same cohort remain below their LPV, with 43% of the 2021 cohort being below that watermark. Furthermore, the complicated cap tables of late-stage private companies pose challenges for companies who need to raise. Many exit-ready companies may prefer taking a down-round IPO rather than a private market down round.”

Source:

State of the Markets - H2 2023 Report

Tweets, Posts, and Charts:

Qubits are insights that we find and share with you.